When Shocks Move

Part 5 of the Sovereign Risk Series

Up to this point, the sovereign framework has been static. Parts 1, 2, 3 and 4 were about what a sovereign is: its monetary position, its real resources, its political capacity, its exposure to external pressure, and the balance between how likely stress is to arrive and how damaging it might be if it does. That positioned each country on a probability–severity plane – a map of where it stands before global conditions shift.

But crises are not static failures. Once pressure actually arrives, it unfolds through time and through institutions, often in ways only loosely connected to the original shock. The same disturbance can be absorbed comfortably in one system and turn corrosive in another that looked stronger on paper. Understanding why requires watching how stress moves once it enters, not just measuring the landscape it lands on.

Korea in late 2022 is a useful place to begin, because it shows what contained stress actually looks like.

Korea is highly exposed by design – capital moves freely, foreign investors hold a significant share of domestic assets, FX markets are deep and liquid, and banks rely routinely on offshore funding. When the US dollar surged in 2022 and US rates repriced faster than most models had anticipated, Korea felt it immediately. The won depreciated sharply over a short period, offshore funding costs widened, and capital flows reversed without friction.

On the surface, this looked like the early stages of a familiar escalation. Currency weakness, tighter funding conditions, and foreign outflows are usually how more serious episodes begin. Yet the process stalled. The Bank of Korea intervened early and credibly, using a small portion of a large reserve stockpile. FX depreciation did not trigger widespread corporate balance-sheet stress. Foreign-currency liabilities were concentrated in export-oriented firms whose revenues rose as the won fell, creating a natural hedge even where formal hedging was incomplete. Offshore funding costs widened but did not choke off bank liquidity, because maturity profiles were manageable and domestic funding remained stable. Crucially, no part of the system was forced into behaviour it would not otherwise have chosen. There was no emergency fiscal tightening, no capital controls, no banking panic, and no political fracture.

The point is not that Korea was calm – it was not. The point is that stress entered easily but did not propagate. It encountered buffers that mattered in the places that mattered, and those buffers absorbed pressure without forcing escalation elsewhere. Low severity, in practice, looks like this: pressure is visible, but choice is preserved.

Italy behaves very differently, and has done so for a long time.

Italian sovereign stress rarely announces itself with a discrete event. It arrives gradually, often dismissed as background noise. Bond spreads widen a little, pause, then widen again. Political coalitions shift, governments weaken, banks look incrementally more fragile, and growth underperforms. Confidence erodes without ever collapsing outright. Nothing snaps, but nothing resets either.

This is not accidental. Past crises have carved deep and persistent channels through the Italian system, and new stress tends to follow those same routes. The sovereign–bank loop is central: banks hold large quantities of domestic government debt, so widening spreads weaken bank balance sheets, which tightens credit, which depresses growth, which worsens fiscal dynamics, which feeds back into spreads. Political fragmentation amplifies this loop because unstable coalitions signal that adjustment will be slow, contested, and incomplete, encouraging markets to price in prolonged fiscal strain and a higher probability that resolution will ultimately require external support. Membership of the eurozone constrains adjustment paths further, removing exchange-rate relief while making fiscal response politically and institutionally costly.

Once pressure enters this system, it does not need to invent a transmission mechanism. It follows paths that already exist, and those paths favour persistence over resolution. Time does not dissipate Italian stress – instead it gives it room to travel. Markets often misread this because they wait for a dramatic rupture that never quite arrives, missing the incremental deterioration that actually defines Italian risk. Severity here is not about speed or spectacle. It is about penetration: how far stress travels once it is inside, how many institutions it touches, and how difficult it becomes to reverse without external intervention.

The UK episode in September 2022 unsettled observers for a different reason, because it showed how quickly stress can compress time when it lands on the wrong structure.

Britain did not look fragile by conventional sovereign measures. Debt levels were elevated but manageable, institutions were intact, the currency was not under speculative attack, the banking system was well capitalised, and monetary sovereignty was unquestioned. The shock itself was not especially large: a poorly judged fiscal announcement that unsettled markets but did not, on its own, imply insolvency or loss of control.

What mattered was where that shock landed. A large segment of the UK pension system had adopted liability-driven investment strategies that relied on leverage and derivative positions tied to gilt yields. When yields rose sharply, margin calls followed. To meet them, funds sold gilts, which pushed yields higher, which triggered further margin calls, forcing more selling. The feedback loop tightened rapidly, compressing what would normally have been a slow repricing into a matter of days.

The Bank of England intervened not because the sovereign was insolvent, but because the market infrastructure was failing. This was a structural shock, not a fiscal one. Leverage had accumulated in a part of the system assumed to be safe, and when that assumption broke, speed replaced depth as the defining risk. The episode was a reminder that modern financial systems can transmit small disturbances with extreme velocity when liquidity promises prove conditional.

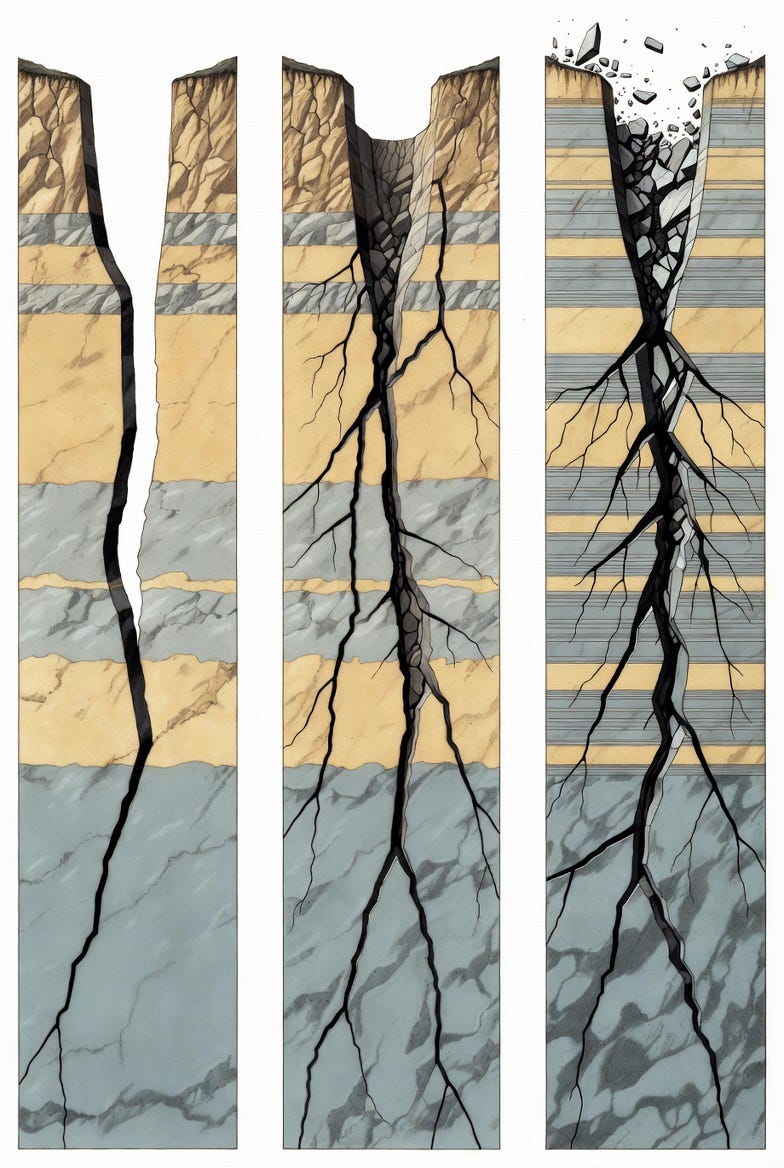

Korea, Italy, and the UK illustrate three distinct propagation patterns.

Korea was easy to reach but difficult to damage. Pressure entered through the external channel, but it met reserves, natural hedges, and stable funding before it could travel further. The system absorbed the shock without surrendering options.

Italy behaves differently. Stress often enters slowly but travels deep, running through political fragmentation and the sovereign–bank loop, reinforcing itself over time rather than resolving. Nothing dramatic snaps; the system simply narrows its own room to manoeuvre.

The UK episode showed how structural fragility can overwhelm fundamentals. Rising yields collided with leverage embedded in collateral chains, allowing a modest fiscal shock to escalate rapidly by collapsing time – shortening the distance between shock and forced behaviour – and converting repricing into liquidity crisis.

What distinguishes these outcomes is not the size of the initial shock, but the alignment between where pressure enters and where buffers or amplifiers sit. In Korea, FX pressure met buffers. In Italy, spreads met entrenched transmission paths. In the UK, yields met leverage.

Propagation depends on whether the active channel encounters forces that dampen stress or forces that amplify it.

Propagation does not replace severity; it describes how severity unfolds. Severity tells you how much damage a shock could do if it reached the system’s vulnerable points. Propagation indicates whether it will reach them, which routes it will follow, and how quickly pressure will accumulate or dissipate along the way.

The question, then, is not simply whether a sovereign looks risky in the abstract, but how it behaves once stress arrives. Does pressure dissipate, embed, or compress time? Does it encounter friction, or does it find channels already prepared for it?

Part 6 turns to that question directly. It sets out how to diagnose these dynamics while they are unfolding, using observable behaviour rather than post-hoc explanation, and how to distinguish containment from escalation before outcomes are obvious.