How Sovereigns Actually Fail

Part 2 of the Sovereign Risk Series

<Brief background and explainer >

Most people picture sovereign failures as fiscal events. A government “runs out of money”. The debt becomes “too high”. Bond markets “lose confidence” and funding dries up. It is neat, intuitive, moral even – it’s also wrong. When a country breaks, it is almost always the result of deeper mechanics: monetary structure, real-world capacity, political resilience, and private balance sheets. Fiscal ratios sit on the surface, but the real vulnerabilities sit below it.

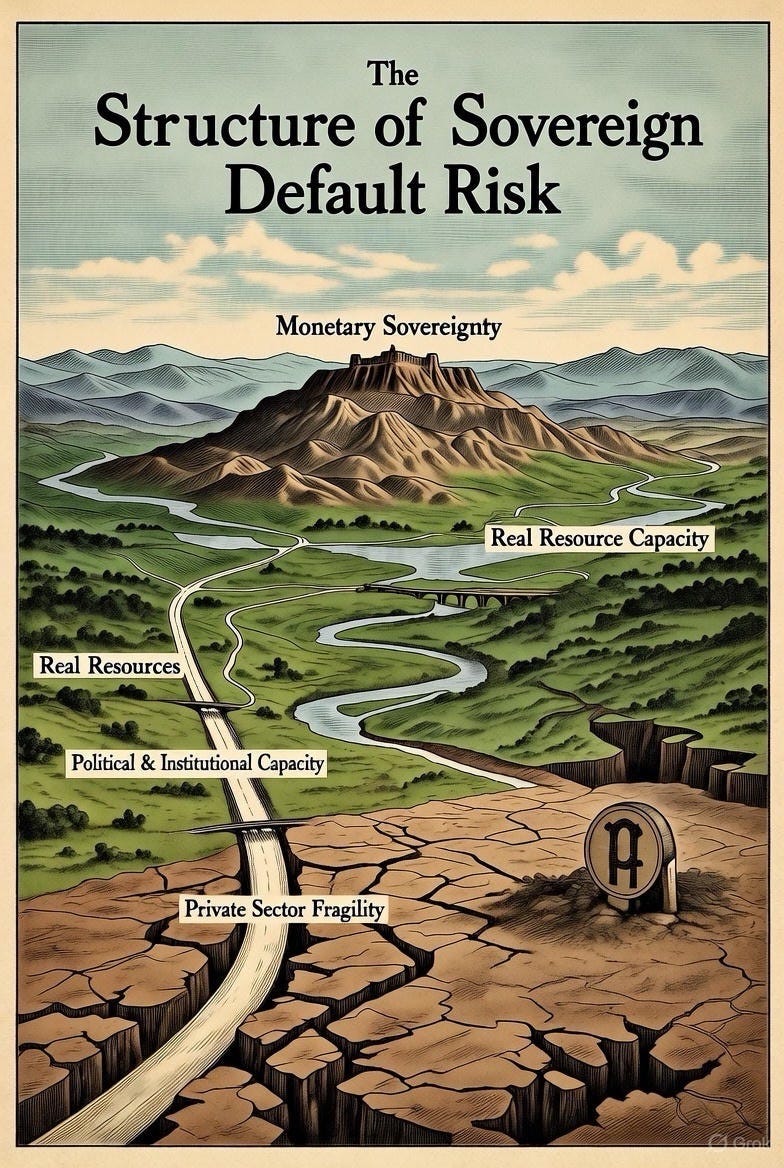

Once you drop the idea that debt/GDP measures sovereign risk, the pattern becomes sharp. Every sovereign stands on four domestic foundations:

Monetary sovereignty

Real resource capacity

Political–institutional resilience

Private-sector fragility

These four forces determine whether a country can absorb shocks, keep its currency stable, and finance itself when the world turns against it. Everything else – spreads, ratings, market drama – is downstream of them.

Let’s take them one by one.

1. Monetary Sovereignty (SBC – Sovereign Balance-Sheet Capacity)

The first question is brutally simple: does the state control the currency it borrows in?

If it does, the logic of default changes completely. A country that issues its own currency, sets its own interest rates, and borrows mostly in that currency cannot run out of it. It can create inflation. It can mismanage credibility. It can debase its exchange rate. But it cannot face an involuntary funding stop in the way a corporation or household can.

This is why Japan and the United States – large debts, slow growth – do not face the risk profile of Greece or Argentina. And why some countries live in a grey zone despite issuing their own currency: Turkey, Brazil, South Africa, Indonesia. They issue domestic currency, but depend heavily on external funding, imported energy, or foreign-currency corporate debt. When conditions tighten, they behave more like currency users than currency issuers.

If you want to understand why debt/GDP generates incoherent rankings, start here. Monetary structure determines whether markets can force a crisis at all.

2. Real Resource Capacity (RRC)

The second foundation asks a physical question: if the government spends more, does the economy generate real output – or hit bottlenecks first? This is the real-world version of fiscal space.

A country with underused capacity can absorb stimulus without inflation. Japan has carried idle labour, dormant investment, and spare production for decades. Extra demand disappears into slack, so if Debt/GDP rises, nothing overheats, and markets discover there was more space than they thought.

A country with structural constraints hits limits early. Australia, Canada, and the UK face hard boundaries in housing supply, energy grids, freight, skilled labour, and basic infrastructure. Extra demand runs straight into these walls. The result is not output, but price pressure. It is a physical limit, not a fiscal one.

This is why countries with low debt/GDP sometimes struggle to run expansionary policy, while countries with high debt/GDP can get away with it. Debt/GDP entirely misses the constraint.

3. Political–Institutional Capacity (PIC)

The third foundation asks whether the political system stays coherent enough to respond when pressure arrives. But this is not about ideology. It is about whether institutions – parliaments, cabinets, central banks, regulatory bodies – remain functional when they are needed most.

Italy shows what happens when this capacity erodes. Its debt has hovered around 120–140% for decades, yet crises recur not because the arithmetic forces them but because governments fall frequently, coalitions fracture, and policy reverses unpredictably. Markets do not worry about the debt stock. They worry about whether any given cabinet will survive long enough to implement its own budget.

The UK’s gilt panic in September 2022 made the same point in real time. Public debt barely moved. What changed was the perception that the state had briefly lost its internal coordination capacity – an abrupt, uncosted mini-budget; incoherent messaging; central bank and Treasury operating on different planes. Markets reacted to the institutional signal, not the fiscal numbers.

Political capacity is time, and weak political capacity burns through it quickly.

4. Private-Sector Fragility (PSF)

The fourth foundation sits entirely off the public balance sheet.

It asks: what does the private sector look like underneath?

Sovereign crises often begin here long before the government accounts show strain. Over-leveraged households, fragile banks, currency-mismatched corporates, and short-term wholesale funding set the stage for sovereign panic.

Ireland did not collapse in 2010 because public debt was high. Public debt exploded because the banking system failed. Spain followed the same pattern. And Australia today carries one of the most leveraged household sectors in the world – a sovereign vulnerability hiding inside mortgage books rather than government ledgers.

When private balance sheets are stretched, any shock quickly becomes a sovereign event. Debt/GDP does not even notice this happening.

Putting the Four Foundations Together

Let’s see how these foundations map onto real sovereigns.

Japan: High monetary sovereignty, persistent slack, strong institutions, cautious private balance sheets. It can absorb enormous shocks. Debt/GDP is noise.

Italy: Constrained monetary position (euro member), moderate real capacity, fragile coalitions, reasonably safe private sector. Crises come from political stress, not public finances.

Australia: Strong monetary sovereignty and stable institutions, but tight resource constraints and extreme household leverage. Vulnerability is not fiscal – it is physical capacity and private debt interacting with external shocks.

Turkey: A currency issuer in principle, but with weak institutions, heavy external financing, and large corporate dollar debts that balloon whenever the lira falls. A constrained issuer where currency shocks become solvency shocks.

These distinctions are obvious once you look at the underlying structure. Debt/GDP cannot produce them.

The Layer Old Models Cannot See

Domestic foundations explain what a sovereign can do, but sovereigns do not operate alone. External forces decide which shocks arrive and how much freedom the state has when they hit. This is where old models fail completely.

Germany in 2022 is the clearest case.

On paper: 60% debt/GDP, balanced budgets, AAA ratings.

In reality: a single point of failure – Russian gas – underpinning its entire industrial economy, plus deep reliance on Chinese demand and US security guarantees. When Russia shut down the gas, the fiscal numbers did not change. The state’s external structure collapsed. Debt/GDP was a spectator.

This is why we need the external layer. Domestic foundations explain resilience, while external exposure and autonomy explain vulnerability.

Where We Go Next

We now have the domestic foundations of sovereign resilience: monetary structure, real capacity, political coherence, and private balance sheets. But sovereignty is shaped as much by what happens outside the border as inside it. External shocks and external constraints determine whether internal capacity is enough.

Part 3 builds that external layer: exposure to global disruption, autonomy to act, and how these interact with the domestic foundations. Once those pieces are in place, the entire sovereign-risk architecture becomes visible – and debt/GDP finally disappears from the conversation.