The World That Pushes Back

Part 3 of the Sovereign Risk Series

Most people imagine sovereigns as if they operate inside sealed containers. A country spends, it taxes, it borrows; the rest of the world murmurs in the background but mostly stays out of the frame. It is an attractive picture because it is simple. It is also wrong. The world has a way of leaning on states, sometimes lightly, sometimes with the weight of a falling beam.

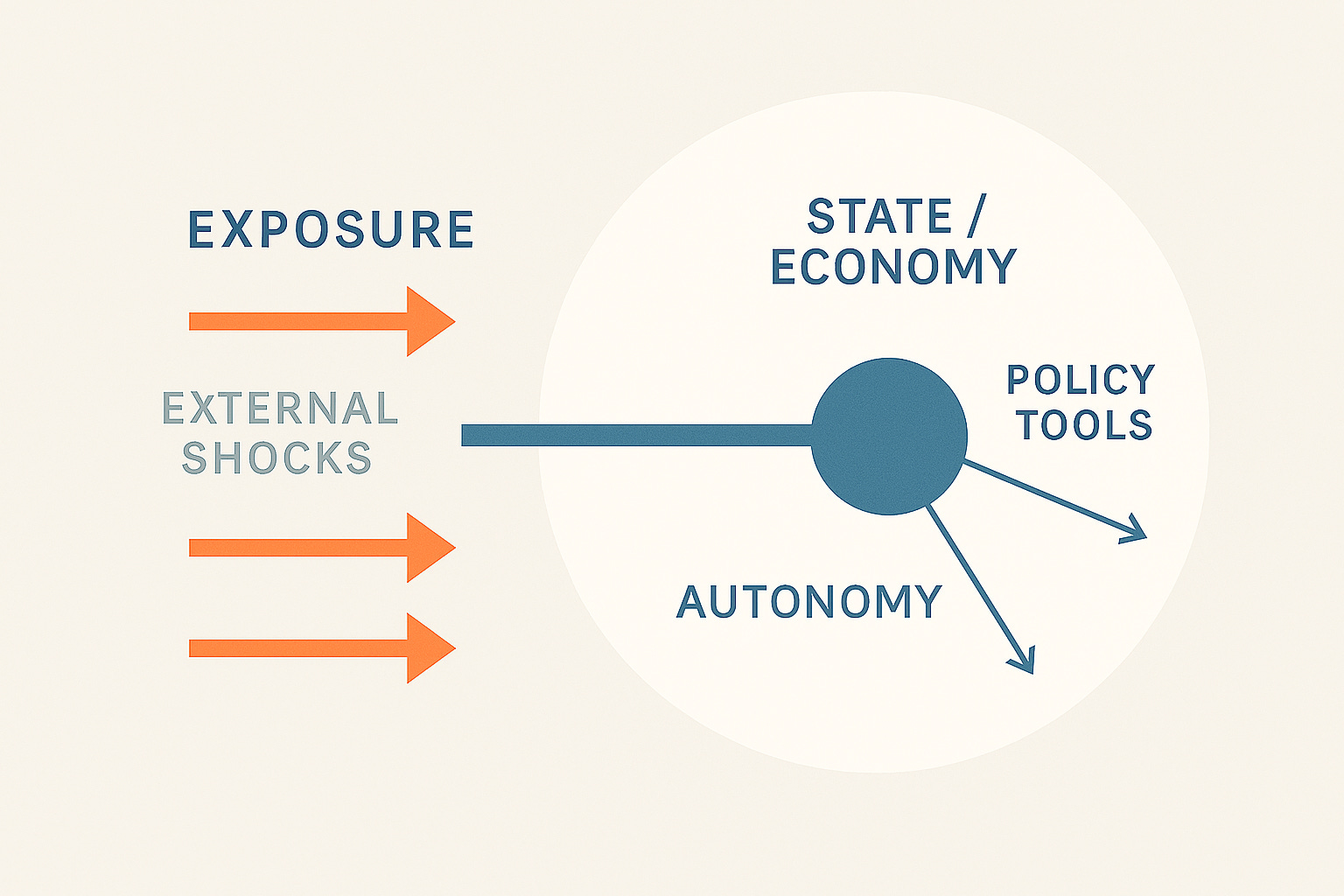

Two things matter here: what hits you, and how much room you have to answer back.

Those forces form the external layer of sovereign risk – the things governments cannot fully control but must live with all the same. Domestic foundations tell you what a sovereign could do under its own steam. The external layer shows you what actually happens when global conditions shift.

To make sense of it, you need to look at two elements: exposure and autonomy. They are related but not the same, and it is their interaction that decides whether a sovereign can absorb shocks or gets knocked sideways.

Exposure: What Hits You

Exposure is the set of forces that reach across borders and strike a sovereign whether it likes it or not. Energy, trade concentration, geography, climate, supply chains – the list is long and uneven, and it only takes one to tilt a country off balance. A state that imports nearly all its fuel lives in a different universe from one that pumps it from the ground. A state that depends on a single trade partner has fewer degrees of freedom than one built on a broad export base.

Energy is the cleanest example because you can see it from orbit. Japan, Korea, most of Europe – all run on imported hydrocarbons. When prices spike, the effects are immediate and physical. It is not about public debt or deficits; it is about whether the grid keeps working and whether industry can function at a tolerable cost. You cannot stabilise an economy if you cannot keep it powered.

Germany offers the sharpest lesson. For years it looked like a model of discipline: balanced budgets, low debt, enviable ratings and borrowing costs. But all of that sat on top of a single assumption – cheap Russian gas flowing through fixed pipelines. When Moscow turned off the tap, the picture changed scale. Germany did not face a sovereign crisis, but it did face something less visible and more unsettling: the sudden realisation that its industrial model rested on a brittle foundation. Fiscal ratios had nothing to say about this. The risk was external and physical.

Trade concentration works in a similar way. Countries tied tightly to one partner – Korea with China, Australia with China, Turkey with the EU – inherit that partner’s business cycle whether they want it or not. A downturn in Beijing is not an event in the spreadsheet; it is a contraction in demand, a fall in earnings, a squeeze on tax receipts and investment. Again, no fiscal measure captures the actual transmission channel.

Climate sits here too, not as an ESG courtesy but as an exposure channel. Water stress, heatwaves, failing crops, rising food import bills – these are sovereign constraints whether or not they appear in the Budget Papers. Sri Lanka shows this in miniature. The collapse began with catastrophic domestic policy choices – most notably the overnight fertiliser ban – but once the economy was off balance, external shocks in fuel, food and tourism amplified the damage far faster than the country could absorb. Climate wasn’t the spark; it was the accelerant sitting behind the wiring.

Supply chains complete the picture. A country that hinges its prosperity on a single critical sector inherits both the advantage and the fragility. Taiwan’s semiconductor dominance is the starkest case. It does not grant security in any conventional sense. What it provides instead is a form of hostage value: the world needs those chips to function, and the consequences of disruption are unthinkable. It reduces some risks and magnifies others. A bright point of failure is still a point of failure.

Once you start tracing exposure, the fiscal ratios recede. They’re not describing the thing that matters anymore.

Autonomy: How Much Room You Have to Answer Back

Exposure tells you what can hit a sovereign. Autonomy tells you what it can do about it. A country with deep policy space can respond to shocks with monetary loosening, fiscal support, market backstops, inventory drawdowns, diplomatic manoeuvres – whatever the moment demands. A country with limited autonomy gets pushed around by events, even when its fundamentals look sound.

The most obvious form of autonomy is monetary. A full currency issuer with deep domestic financing – Japan, the United States, to a lesser extent Canada – can intervene forcefully when shocks arrive. It can stabilise markets, support banks, lean against recessions and buy time for structural adjustment. None of this guarantees success, but it buys room.

Currency users have no such luxury. Eurozone states can borrow in what is technically “their” money, but they do not control the issuer of that money. Their autonomy is partial at best, conditional on the ECB and on the politics of nineteen other governments. It is a strong system in normal times and a fragile one in abnormal times. Italy can run deficits, but it cannot unilaterally determine the terms of liquidity support.

Geopolitics also shapes autonomy more than most models admit. South Korea is a wealthy, sophisticated country, but its room for manoeuvre is narrow. Its security dependence is asymmetric, its trade exposure is lopsided, and its strategic geography is unforgiving. When the world shifts, Korea feels it early and hard. Formal monetary sovereignty cannot fully offset this.

Turkey is a different story. Its autonomy problem is self-made. A once-credible central bank was sidelined, then bent, then hollowed out. Interest-rate policy became a loyalty test. Corporate balance sheets filled with dollar debt, setting the trap: every fall in the lira detonates liabilities faster than policy can respond. The currency is sovereign in name but not in practice.

Autonomy by itself is only half the story; exposure by itself is noise.

The interesting part is what happens when they collide.

The Interaction: Where Crises Actually Emerge

Some combinations break quickly. High exposure with low autonomy – Thailand in 1997, Indonesia in 1998 – is where systems snap. Shocks arrive, policy space evaporates, markets run, and the crisis becomes self-propelling. You can survive high exposure if you have room to act, and you can survive low autonomy if the world leaves you alone. You cannot survive both at once.

Some combinations muddle through for years. Moderate exposure with limited autonomy is uncomfortable but manageable – you get volatility, you get political noise, but not collapse. Much of Latin America lives here.

Then there are sovereignties that bend without breaking. High exposure, strong autonomy. Japan has lived in this quadrant for decades. Energy importer, ageing population, trade exposed, supply-chain dependent – and yet extraordinarily resilient because its monetary and political institutions can absorb and redirect shocks.

And then there are the quiet cases: low exposure, high autonomy. Canada most years, New Zealand, parts of Scandinavia. These sovereigns feel the world’s gusts but rarely its storms. They are not immune; they are insulated.

Australia should sit here too, but two features drag it across the matrix. First, a private sector built on extraordinary leverage – variable-rate mortgages, banks reliant on offshore wholesale funding, household debt pushing 180% of income. Second, a business cycle tied tightly to China’s demand for commodities. Not fatal exposures, but narrow margins that matter when shocks arrive.

The external layer does not replace the domestic foundations. It tells you how those foundations will be tested, and where they might fracture. A sovereign with strong internal capacity but brittle external dependencies will surprise you in a very different way from one with fragile institutions but a forgiving external environment.

Part 4 takes this one step further. Exposure and autonomy tell you how shocks land – but they do not yet tell you how often shocks turn into crises, or how severe those crises become. For that you need the probability and severity layers. Those are where the system, finally, comes together.