The Diversification Illusion

Diversification shifted the source of oil, but it did not shift the vulnerability

Daniel Yergin is one of the most authoritative voices in global energy. His book The Prize remains the definitive history of the oil industry, and his Pulitzer reflects a career of serious analytical work. Experts are not infallible, however, and his piece in the Wall Street Journal this week gets the diagnosis half right and the conclusion wrong.

He is right that the world has more sources of oil than it did in the 1970s, and right that diversification has moderated the first-round shock. Where the argument fails is in treating moderation as resilience. They are not the same thing, and the difference between them is where the real analysis starts.

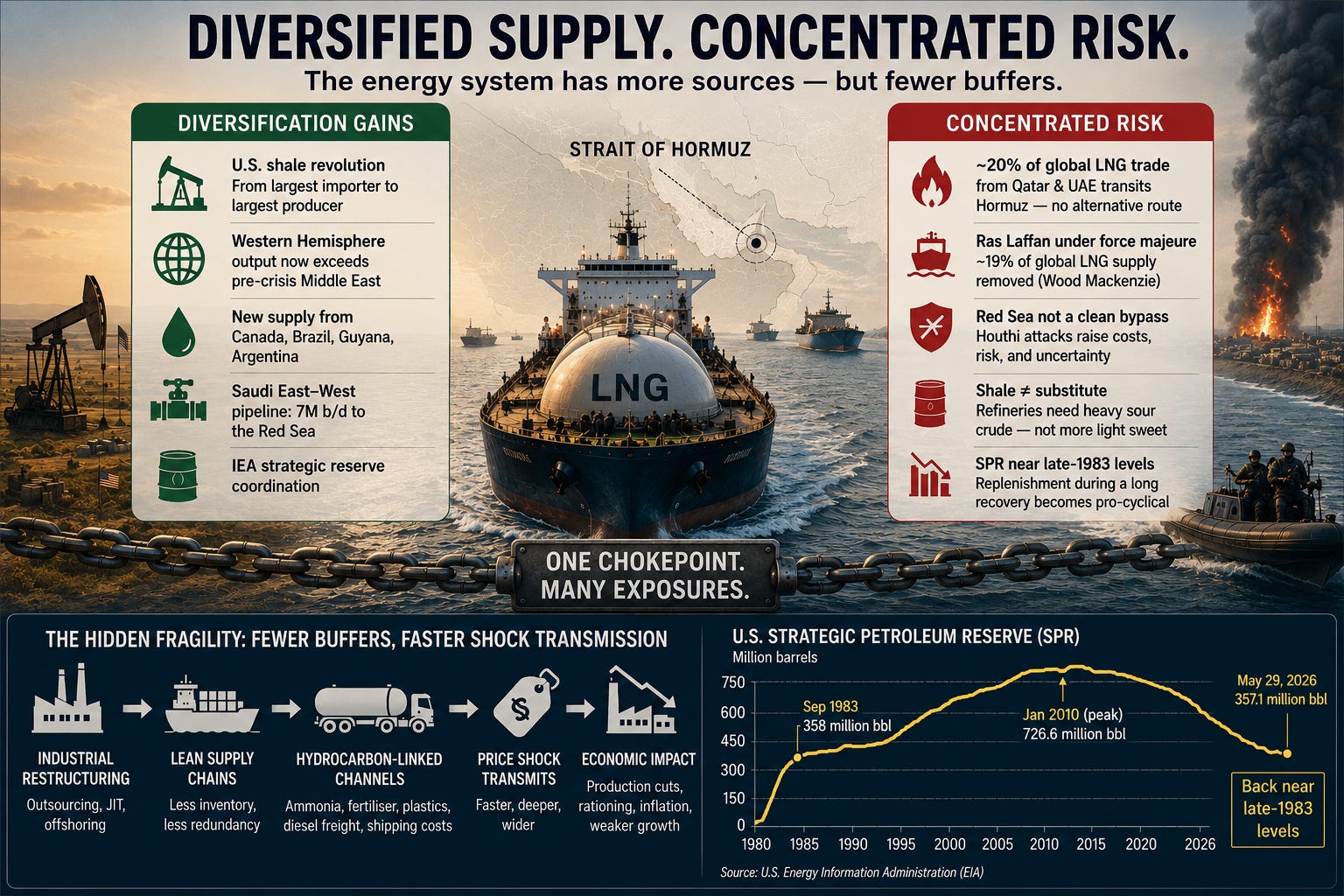

Yergin’s case rests on what he calls the Churchill axiom – “safety and certainty in oil lie in variety alone.” He traces the diversification gains of the past half-century: the shale revolution transforming the United States from the world’s largest oil importer to its largest producer, and Western Hemisphere output now exceeding what the Middle East produced before the crisis, with Canada, Brazil, Guyana, and Argentina all adding supply. The Saudi East-West pipeline moving 7 million barrels a day to the Red Sea. The IEA coordinating strategic reserve releases. The implication is that the architecture built after the 1970s crises is doing its job. In the narrow first-round sense, that is true. Diversification has moderated the shock, but it has not proved the system resilient.

What this misses is where the vulnerability went.

Rather than eliminating its hydrocarbon dependence after 1973, the world restructured it. Oil was partially displaced by gas, and gas became a critical industrial feedstock for Europe and Asia in a way oil never fully was. LNG is now one of the central fuels for electricity generation in Japan and South Korea, and a significant industrial input across continental Europe. LNG exports from Qatar and the UAE through Hormuz represent almost one-fifth of global LNG trade. That supply has no pipeline bypass, no strategic reserve equivalent, and – for buyers under long-term Qatari contracts – no immediate alternative. Yergin cites Japan’s pivot to LNG as one of the diversification successes of the post-1970s era, without noting that LNG itself has become exposed to the same chokepoint logic the pivot was meant to escape. Qatari LNG exports have been operating under severe constraint since early March, with force majeure declared from Ras Laffan. Wood Mackenzie – an S&P Global company – assessed the strikes on Ras Laffan as removing approximately 19% of global LNG supply from the market and described the damage as fundamentally reshaping the global gas outlook. Yergin is vice-chairman of S&P Global, yet its analysts reached the opposite conclusion.

There is a further problem with the pipeline diversification Yergin cites. The Saudi East-West pipeline moves oil west to Yanbu on the Red Sea, but barrels leaving Yanbu still face the southern Red Sea and Bab el-Mandeb risk environment, where Houthi attacks since late 2023 have raised war risk insurance costs, reduced vessel availability, and complicated routing. The bypass shifts the chokepoint from Hormuz to a different contested waterway rather than eliminating it.

LNG shows the immediate flaw in the diversification story: supply was diversified away from oil, but not away from chokepoints. The wider problem is that the same half-century also stripped out the industrial buffers that once slowed energy shocks before they reached final output.

The post-1970s industrial restructuring – outsourcing, just-in-time logistics, and offshoring of petrochemical-intensive manufacturing – reduced the energy line on corporate income statements while embedding hydrocarbon exposure more deeply into supply chains. Companies appear less oil-dependent because they consume less energy directly, yet their inputs, components, and logistics are often more exposed to energy price shocks than the headline figures suggest. Ammonia and fertiliser production, plastics, diesel freight, and shipping costs are hydrocarbon-linked channels through which an energy shock moves into food, manufacturing, and distribution long after the crude price itself has stabilised. The buffers that existed in a 1970s industrial economy – company inventory holdings, domestic manufacturing capacity, and slack in logistics networks – were engineered out as deliberate efficiency gains. A 1970s economy absorbed shocks through inventory drawdown before they reached the production line, but the 2026 economy transmits them almost immediately.

Yergin also invokes US shale production growth as a diversification success – and it is, in volumetric terms. But US shale produces predominantly light sweet crude, and refineries configured around medium and heavy sour Gulf grades cannot substitute one for the other without yield, margin, and logistics penalties. Senior industry executives, including Chevron and ExxonMobil’s, have flagged oil prices well above current levels as the inventory and recovery arithmetic becomes apparent. More barrels do not help if they are the wrong barrels for the refineries that need them.

Yergin’s treatment of strategic petroleum reserves (SPR) follows the same pattern – correct in institutional terms, incomplete in current application. The SPR was designed as a counter-cyclical instrument: release inventory during supply shocks, then refill gradually in well-supplied markets where additional government demand does not move prices. That cycle depends on disruptions being short and sharp, with a clean return to normal supply. What is happening now inverts the design logic entirely. Reserves have been drawn down at record rates during the disruption – the US SPR is back near levels last seen in the early-to-mid 1980s. When governments eventually refill, they will be buying into a market simultaneously absorbing three other demands: commercial inventory rebuilding, Asian strategic and commercial reserve restocking after months of severely reduced imports, and supply still recovering along the curve Sultan Al Jaber, CEO of ADNOC, described – 80% of pre-war Gulf flows at four to six months after reopening, full normalisation not until Q1 or Q2 2027. Strategic reserve replenishment adds a fourth source of demand competing for the same recovering barrels at precisely the moment political pressure to rebuild visibly is highest. Instead of dampening the price cycle as designed, SPR replenishment amplifies it. The instrument becomes pro-cyclical rather than counter-cyclical.

The recovery arithmetic undermines his price scenario. Yergin writes that if the strait opens soon, prices will come down – then, three paragraphs later, cites S&P Global’s own analysis that it would take up to six months to return to 80% of pre-crisis supply after reopening. He states the evidence but does not follow it to its conclusion. If the recovery ramp runs to six months or beyond, the inventory drawdown continues through the recovery period, commercial and strategic restocking compete for constrained supply, and prices do not normalise on reopening. They normalise only when the recovery ramp, commercial restocking, and strategic reserve replenishment are absorbed, which is not the scenario the current futures price is pricing, and not what “prices will come down” implies to a reader.

Yergin argues that markets contribute to energy security by adjusting faster than governments, citing the 1970s gas lines as a failure of price controls rather than of the underlying supply. That is partially correct as history, but the wrong lesson for a physical shortage of this scale. Market adjustment under severe supply constraint means price rationing – prices rise until demand falls to match available supply – and at this level of disruption, what the market clears is economic activity. Governments across Asia are already rationing, issuing work-from-home directives, and prioritising domestic consumers over industrial users not because they misread the 1970s but because the alternative is pricing ordinary households and manufacturers out of energy entirely. Demand destruction is not resilience.

The post-1973 system diversified supply, but it also reduced inventory, redundancy, and domestic industrial slack. It made the energy system broader, but not more shock-resistant. Diversification shifted the source of oil; it did not diversify away from chokepoints, did not restore the grade flexibility that heavy sour Gulf crude provided, did not create an LNG strategic reserve equivalent, and did not anticipate a recovery curve long enough to turn its own counter-cyclical instruments pro-cyclical. Yergin is right about diversification – and wrong about what diversification proves.