The Resolution Premium

Three paths from here. The market is priced below the most favourable one.

Brent crude is trading around $105 per barrel – a resolution-premium price reflecting a market assigning high probability to early diplomatic resolution and discounting the physical data almost entirely. The three paths from here differ not in direction but in duration, and duration is what determines whether the damage is severe or historic.

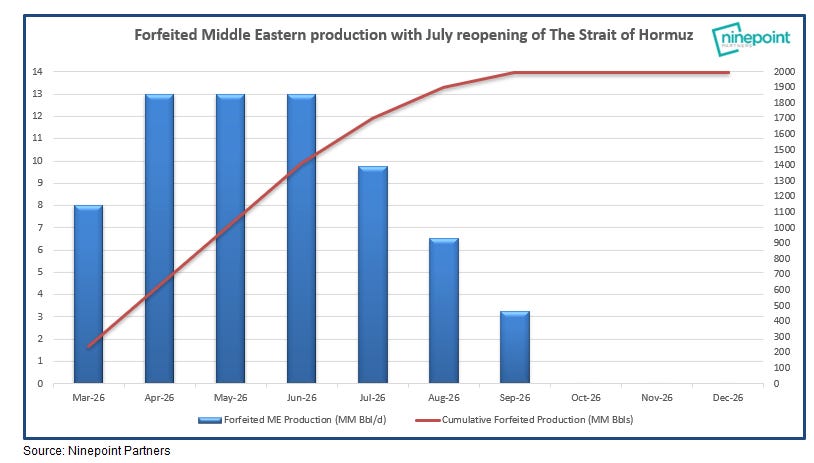

The favourable path has Hormuz reopening in June or early July, which is what current pricing implies, but reopening and restoration are different things. Sultan Al Jaber, CEO of ADNOC, stated publicly that Gulf oil flows would take at least four months to recover to 80% of pre-war levels even under immediate resolution – meaning a July reopening produces approximately 20 mb/d of flow by November, still 5 mb/d short of the pre-war baseline, and cumulative forfeited Middle Eastern production reaches approximately two billion barrels before normalisation, a volume the global inventory system cannot readily absorb.

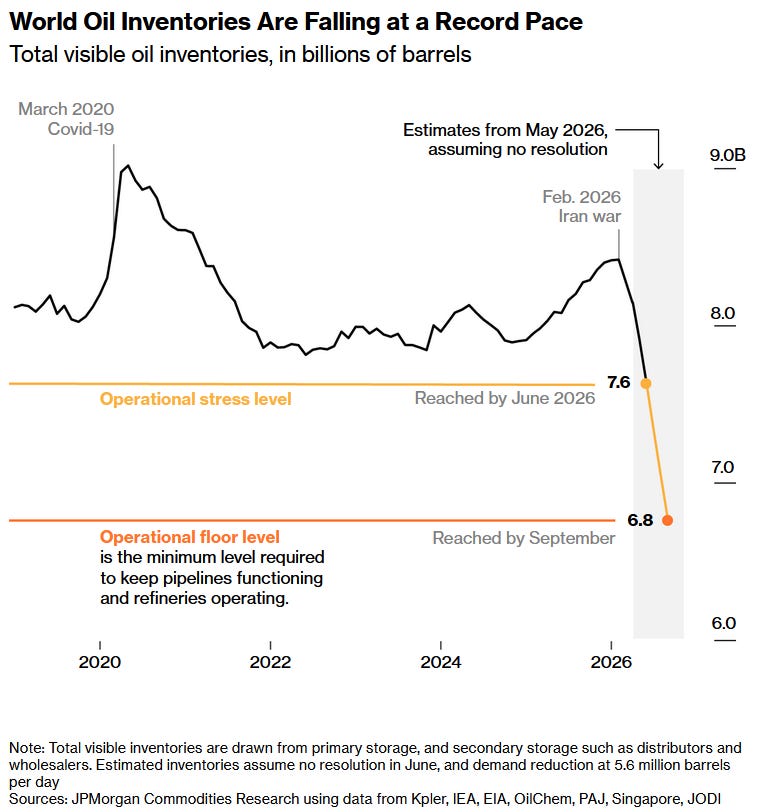

The JPMorgan inventory analysis puts total visible global inventories hitting operational stress level – 7.6 billion barrels – in June, with the operational floor, below which pipelines and refineries begin to encounter feedstock difficulty, arriving in September at 6.8 billion barrels. A July reopening slows the draw but does not stop it, and Q2 corporate earnings, reported from July, will be the first illustration of the feedstock constraint appearing in industrial results rather than energy sector data alone.

The AI investment cycle bifurcates in this path in a way that determines how much of the damage the advanced economies absorb. Pre-war, the hyperscaler capex boom was adding an estimated 0.3 percentage points to annualised US growth – and if financial conditions stay loose enough to sustain it, that investment provides a partial offset, not enough to cancel the energy shock but enough to prevent the US tipping into outright recession. If the energy shock and the bond market sell-off tighten conditions sufficiently to interrupt the circular financing arrangements that underpin hyperscaler debt issuance, that offset disappears and the growth picture darkens considerably even under early resolution.

Price in this path: Brent in the $120-160 range, peaking as the inventory draw continues into June and July before declining through Q4 as flows recover. The market is currently below this floor, meaning even the best case involves prices rising from here before they fall.

The middle path has Hormuz not fully reopening until late July or August, with resumption gradual rather than clean, as tanker operators, insurers, and cargo owners will not return to normal liftings on the day a ceasefire is announced and mine clearance, cargo insurance reactivation, and infrastructure certification each add weeks to the ramp-up. The two billion barrel cumulative forfeit is reached and exceeded before flows recover, and the inventory floor approaches in September.

The price arithmetic – worked through briefly here and in detail in a subsequent piece – puts the market-clearing price for a sustained 12-15% supply shortfall in the $180-240 range, with the floor set by the optimistic end of the demand elasticity estimates and the ceiling reflecting financial amplification adding a risk premium on top of physical scarcity as the closure extends. The market at $105 is priced below even the most favourable scenario, and the gap to the middle path’s floor is nearly double the current price. That gap will not close gradually as sentiment shifts – the oil price will increase significantly and rapidly when the physical shortage can no longer be deferred by inventory draws.

The central bank bind tightens here independently of the energy price – inflation stays elevated on energy and feedstock costs while growth contracts, closing the standard policy exits simultaneously, since rate cuts add to inflationary pressure while rate holds deepen the recession. The stagflation configuration turns from a tail risk to a base case, and the policy timeline that would otherwise resolve it extends with every week the strait stays closed.

The same AI bifurcation applies in this path, but at a worse baseline, because financial conditions tightening from extended closure is the environment in which the circular financing arrangements the IMF’s April 2026 Global Financial Stability Report identified as fragile are least likely to survive. The hyperscaler capex boom, which pre-war was absorbing surplus global capital and driving technology investment across the sector, becomes a vulnerability rather than an offset. The IMF’s own scenario analysis suggests that if AI investment falters it removes one of the two remaining pillars – the AI investment tailwind and the market’s assumption of early permanent ceasefire – supporting current equity market levels.

Price in this path: Brent in the $180-240 range for an extended period. The Dubai cash market – which prices physical crude for immediate Gulf delivery – briefly hit $166-170 on 19 March, suggesting the lower boundary of this range has already been touched in physical spot markets while the forward market has not caught up.

The worst path has closure persisting into the second half of the year. This will result in a breach of the inventory floor and refinery feedstock stress appearing in industrial output. It will manifest not as a consumer energy price effect, but as a physical availability constraint on production, with price dynamics turning non-linear as inventories fall below working minimums and buyers compete for available barrels regardless of cost.

Price in this path: The $260-320 range follows from the arithmetic of a sustained physical shortage – at the lower estimates of how much demand falls when price rises, clearing a 12-15% supply shortfall requires a price increase of 240-300% from pre-war levels, and financial amplification adds a further premium once the inventory floor gives way.

The reason this path is not merely theoretical is that it does not depend on a negotiating gap – these close when the price is right, but a deal also requires someone with the authority to make it stick. That person does not currently exist in Tehran – the internal arbitration mechanism to translate any agreement into binding action is missing. This mechanism had converted competing institutional pressures from the IRGC, the presidency, the clerical establishment, and the remaining hardliner faction into unified decisions. It was exercised by Khamenei for four decades, but was removed when he was killed in the opening days of the conflict, nothing has replaced it, and it does not respond directly to external pressure or economic pain. The negotiating gap is also too wide to bridge regardless of institutional capacity – disagreements over nuclear and enrichment issues – but the arbitration problem means that even a narrower gap would not currently produce a deal that binds anyone.

The AI question is moot in this path – the shock overwhelms any potential offset.

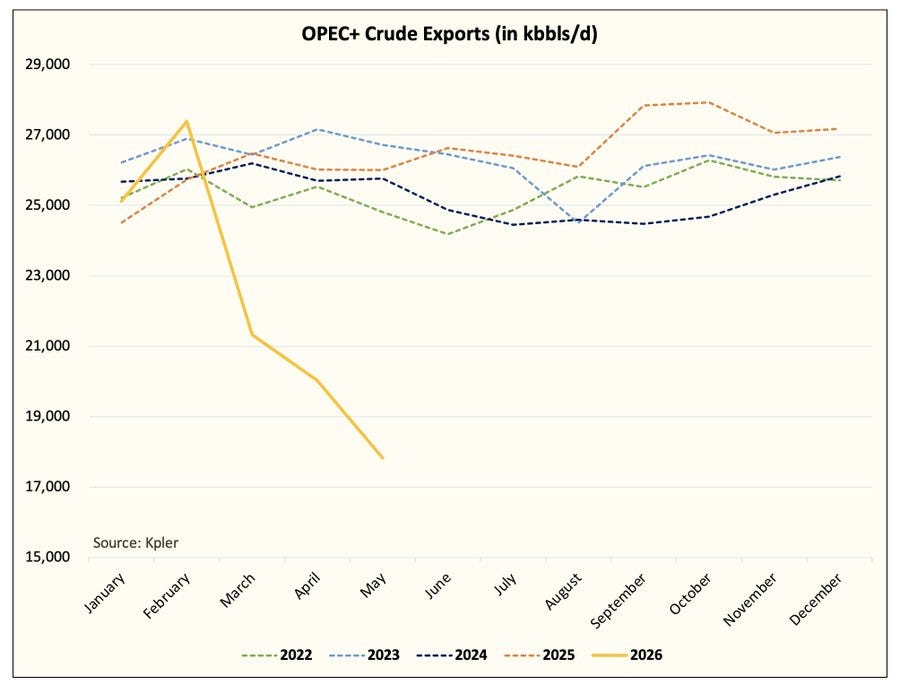

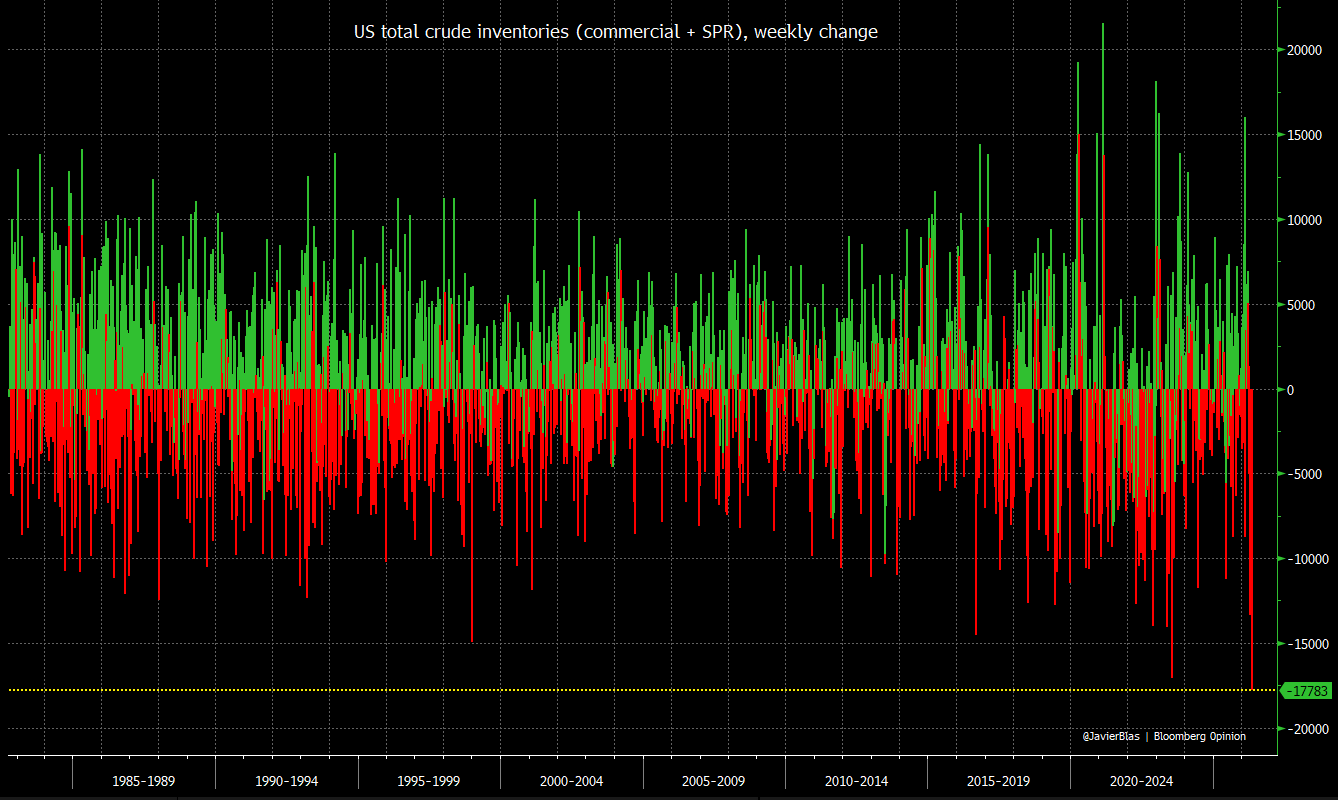

The current data puts the market at a price below the favourable path while the physical reality runs on the trajectory of the middle one. Kpler shipping data shows OPEC+ crude exports at approximately 17.8m bbls/d in May against a pre-war baseline near 25.0m, with the 2026 export line falling entirely outside the 2022-2025 range. US total crude inventories – commercial and strategic combined – drew 17.8 million barrels in a single week, the largest weekly draw in more than forty years of recorded data. Mohamed El-Erian noted on 17 May that for almost three months the true scale of the energy supply deficit had been masked by an extraordinary drawdown of global crude stockpiles.

On 20 May, Brent dropped nearly 5% on a single Trump statement about negotiations being in their “final stages”, even as Hormuz remained physically closed and the weekly draw continued at record pace – the market updated on the signal rather than the condition, which is the resolution premium at work. That gap between financial pricing and physical reality closes in one of two ways: resolution arrives before the inventory floor forces it, or the inventory floor forces it regardless, and the JPMorgan timeline puts the forcing window between August and October.

I struggle to understand why people fail to acknowledge the possibility of forced demand destruction. It is already happening in other parts of the world, why not to Europe or US?