Two Prices, One Barrel

The futures curve says the energy crisis is nearly over. The inventory data says the worst is still ahead.

FT Alphaville put the essential point in one sentence in March: most oil traders don’t trade oil. The benchmarks everyone cites – Brent crude, WTI – are futures prices. A futures contract is an agreement to buy or sell a commodity at a fixed price on a future date, and the traders who buy and sell these contracts mostly never take delivery of a barrel. The vast majority of futures volume settles in cash. What these markets are trading is not oil but a bet on the likelihood that oil will be available at a given price on a given date. Price volatility in these markets, as Alphaville noted, is “a measure of how difficult it is at any given moment to suppress the knowledge that no one knows anything”.

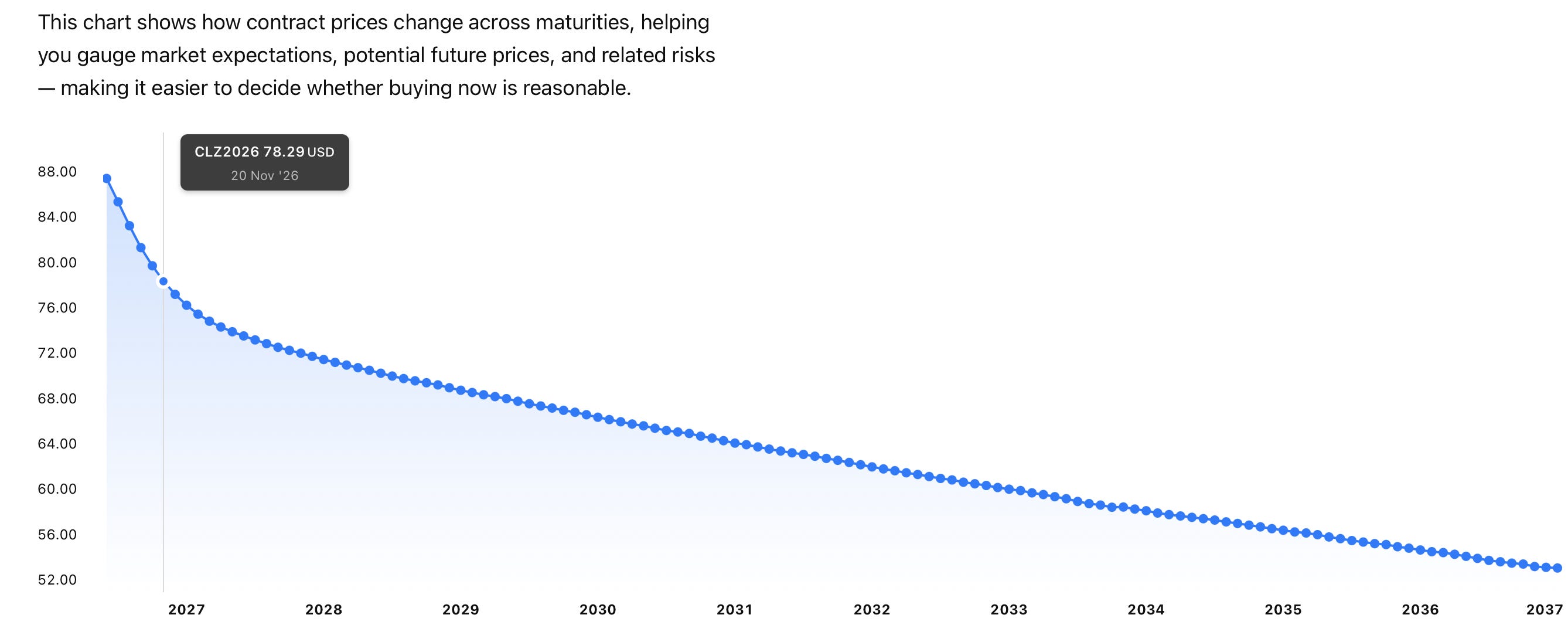

Understanding this is crucial right now, because the deal – the Iran-US memorandum of understanding (MOU) to end the war that has severely disrupted flows through the Strait of Hormuz (roughly one-fifth of global oil consumption) and begin negotiations on Iran’s nuclear programme and sanctions – is being priced into the futures market in a very specific way. Brent crude futures have fallen from approximately $117 to $87 over the past two months.

Robin Brooks has made a specific and apparently evidentially grounded claim: futures were right. Paper prices anticipated the ceasefire and the deal, the premium for immediate barrels fell, and Dated Brent – the real-world benchmark for physical North Sea crude – then fell toward futures rather than the reverse. The collapse in the spread between physical and paper prices proved, on his account, that the acute physical scarcity argument was overpriced. He has set a target of $85 for Brent on a peace deal and argues the market is rapidly approaching it. That interpretation gets the direction of the April price move correct, but it over-reads what that move proves.

The forward-looking logic behind that conclusion is correct in principle. A futures contract for July delivery is not priced for today’s shortage but for what traders expect conditions to be in July. If they expect the deal to reopen Hormuz before then, the July contract is priced for a post-deal world. That reasoning is sound, yet it rests entirely on the timing assumption being correct, and on correctly understanding what the shape of the futures curve is actually measuring.

Boston Consulting Group analyst Jamie Webster has set out the key distinction. Backwardation – when near-term delivery prices are higher than prices for future delivery – measures immediate physical scarcity, not optimism about future stability. As Webster explains, “the greater the need for barrels today, the stronger the downward slope in the curve becomes”, creating pressure to release oil from storage and deliver immediately. It does not mean the market expects prices to fall; it means physical buyers are paying a premium to secure supply now – each available barrel, in the formulation of Gianluca Benigno, professor at the University of Lausanne, “begins to trade less like a commodity and more like insurance”. When arguments suggest a “near-total collapse” of that backwardation, they show that the insurance premium has fallen, not that the physical shortage has resolved. Insurance premiums fall when confidence about future delivery rises. The deal optimism priced into the futures curve is the mechanism by which the premium compressed, and that is not the same thing as proof that the deal will deliver on the schedule the curve is pricing.

The question the curve cannot answer is whether that confidence is warranted. Martin Wolf, writing in the Financial Times on 20 May, put it directly: “Yes, the oil futures markets suggest that prices are set to fall and so all will be well. But the oil futures curve is not a crystal ball, as my colleagues Jonathan Vincent and Malcolm Moore have noted.” FT’s Vincent and Moore stated that lower prices for crude to be delivered at a later date do not mean traders are predicting a sharp fall. The academic literature is equally clear. Ron Alquist and Lutz Kilian, studying two decades of oil futures data, found that futures-based forecasts are no more accurate than simply assuming the current spot price will persist, at any horizon up to twelve months. BP’s chief economist stated the practitioner view simply: “We cannot forecast oil prices with any degree of accuracy over any period whether short or long”. The futures market’s record of pricing normalisation before it arrives – and being surprised when it doesn’t – is not reassuring.

The physical market tells a different story to the paper one. During the acute phase of the crisis, before the April ceasefire and the deal optimism that since compressed the backwardation, several refined products – diesel, jet fuel, naphtha – traded above $200 per barrel, according to Webster’s analysis. Clyde Russell, writing for Reuters, observed that Dubai cash-settled cargoes were trading at a wide premium to the equivalent futures swaps – anecdotally, up near $160-170 – and that paper traders appeared “more confident than oil consumers about a quick ceasefire and manageable supply disruptions” in a way that “seems untethered from the reality on the ground”.

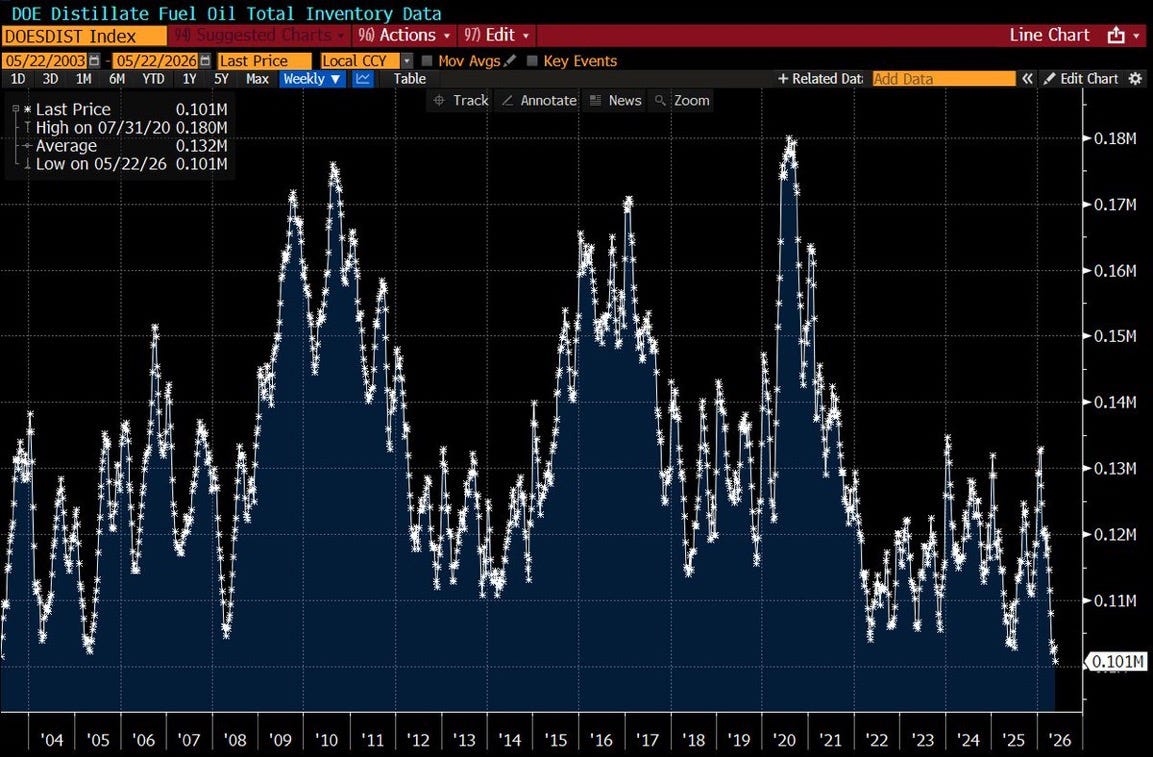

US distillate inventories – diesel, heating oil, and jet fuel precursors – stand at their lowest level since at least 2003 in the Bloomberg/DOE series, 24% below the long-run average. Neil Chapman, Senior Vice President of ExxonMobil, said at a Bernstein conference this week that inventories are approaching “unheard of” levels and that once they hit their floor, “dated Brent, a model would say, will shoot up to $150, $160.” His timeline is two to three weeks.

A market pricing $87 oil is implicitly assuming that physical normalisation arrives before inventory floors become binding. The physical data does not disprove that assumption, but it makes the assumption a very large one. The insurance premium fell because confidence in future delivery rose, not because the physical shortage resolved. The distillate inventory level, the refined product premiums during the acute phase, the massive drawing of strategic reserves, the JPMorgan forecast of the approaching operational floor, and Chapman’s observation all suggest the inventory floor is reached before the normalisation the futures curve is pricing. If that sequencing is right, the confidence that drove the premium lower proves misplaced and the premium returns. The buffers that have been absorbing the supply shortfall – the Strategic Petroleum Reserve, coordinated IEA emergency releases, commercial inventory drawdowns, demand management in Asia – are approaching exhaustion. Once they cease, the premium for immediate barrels cannot continue to fall. Physical buyers who need actual barrels cannot pay with probability weights on a future deal.

Brent futures do not float free of the physical Brent complex. As contract expiry approaches, the paper price has to converge on the physical market through the settlement and expiry mechanism, and that convergence can run in either direction. In April it ran downward: Dated Brent, S&P Global Platts’ daily physical benchmark assessment for prompt North Sea crude, fell toward futures as deal confidence rose. If the deal has not delivered actual barrels by the next settlement window, that same convergence mechanism runs upward, toward wherever the physical benchmark is trading when contracts expire. The April convergence that Brooks correctly identified as closing from the top works symmetrically. If the confidence that compressed the insurance premium proves misplaced, the premium returns and convergence runs the other way.

Sultan Al Jaber, CEO of ADNOC stated that even an immediate opening of the Strait does not restore full pre-war flows until Q1 or Q2 2027, and that it would take at least four months to return oil flow to 80% of pre-war levels. He also told the Atlantic Council that the world drew down approximately 250 million barrels from storage in just two months and that 30 to 35 days of effective cover remains. That is a clear articulation of the specific interval between the current futures price and the physical reality.

Whether the deal delivers on the timeline the $87 futures price implies is a question the curve itself cannot answer. That answer comes from ship traffic through Hormuz – still near zero – from inventory levels, and from the operational timelines that Sultan Al Jaber and Chevron CEO Mike Wirth have described. All of those point in the same direction: the insurance premium fell faster than the physical reality justified.

Postscript

Yet again we have an announcement that the US and Iran are nearing an agreement to sign the MOU. At best that is a deal to agree to a deal to agree to defer the discussion about a deal after another ceasefire that extended the multiple previous ceasefire extensions.

After the announcement Trump backed off again, saying he wasn’t ready to sign yet, while Tehran stated that the terms announced by the US were nothing like the terms it had agreed to. Deja vu.