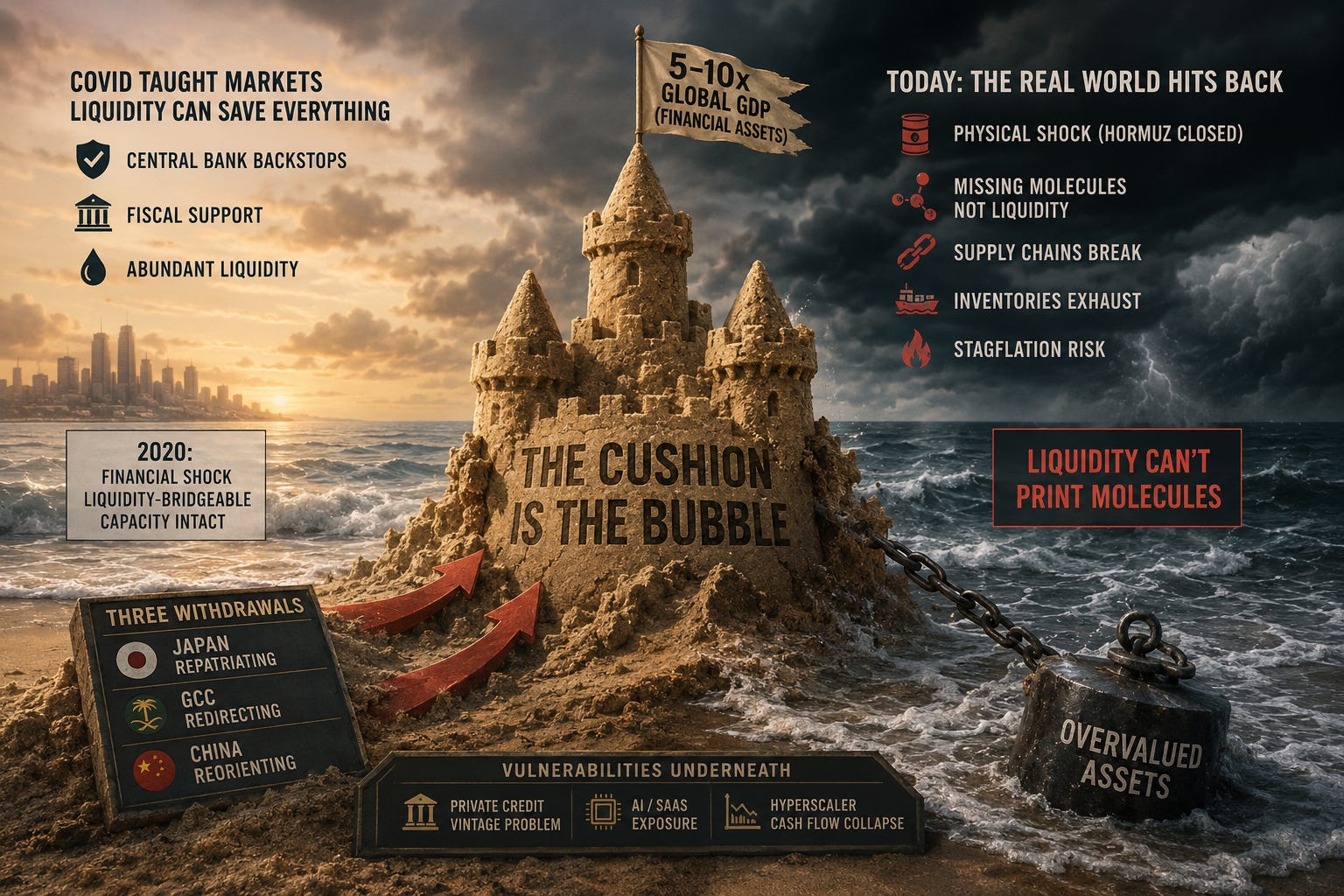

The Cushion Is the Bubble

Markets are pricing a financial fix for a physical problem, but when the shock is molecules rather than money, the central bank playbook does not apply

On Saturday the AFR’s Chanticleer featured observations by Viktor Shvets and Matt King, two serious analysts agreeing on the same uncomfortable diagnosis: markets are frothy, momentum has replaced fundamentals, and professional investors know the rally is fragile but keep buying anyway. However, the comfort they draw from this picture is where the analysis goes wrong.

Shvets argues that the financial system cushion – capital running at five to ten times global GDP – gives markets an enormous buffer against correction, while King warns that correlation risk makes a momentum reversal dangerous, concedes that a further ‘melt-up’ pulling in more late money is equally plausible on any given week, and leaves open what actually arrests the cycle. Both are diagnosing the same trap – the market knows the structure is fragile but cannot prudently sit out – yet neither asks the pertinent question of whether the cushion is what it appears to be.

A second Chanticleer piece, published yesterday, responds to Wall St’s “nasty fall” on Friday, identifying the two most likely bubble poppers as rising interest rate expectations and hubris around AI spending. Unexpectedly hot US jobs data forced markets to price a Fed rate rise before year end, while SpaceX’s equity raise – with pricing set for 11 June and trading beginning 12 June – Meta’s rumoured capital call, and Google’s $80 billion tap of equity markets all signalled that the hyperscalers can no longer fund AI capex from their own cash flow. The analysis is correct on the financial mechanics, but what it does not address is why the interest rate pressure is stickier than previous episodes and why the AI capex squeeze is harder to relieve. The answer to both lies outside the financial system, in a physical constraint that the usual rate cut solution cannot solve.

The five-to-ten-times figure Shvets cites appears to be the aggregate stock of financial assets – equities, bonds, derivatives, bank assets, and shadow banking vehicles – measured against annual global output, but the problem with it is that inflated asset prices are included in the numerator. The cushion therefore incorporates the very thing it is supposed to cushion against: when equity markets fall 40%, the financial capital ratio falls with them, and the buffer shrinks at the moment it is needed most. Shvets is using the bubble as evidence of the safety net, but it is undermined by the circularity running through it. The capital stack is a sand castle: bonds, derivatives, and private credit built on fifteen years of compressed yields and abundant foreign capital, both of which are now withdrawing.

What Shvets is pointing to is a stock of claims, yet the real backstop in a crisis is not a stock but a power – the authority central banks hold to manufacture settlement liquidity and lend against distressed assets. No pre-existing pile of capital is needed for that; what is needed is political permission, fiscal headroom, and tolerance for inflation, and all three are narrower now than they were in 2020.

Covid created that confusion. Markets broke in March 2020 as the ‘dash for cash’ reduced J.P. Morgan’s Treasury market depth – how much of a security you can buy or sell without moving the price – to only $12 million against a normal of hundreds of millions, and the repo market that funds leveraged positions using those Treasuries as collateral was at the edge of seizure. The Fed rescued the entire market-based finance system by backstopping it, while governments replaced lost household and corporate income at levels normally associated with wartime. The result was not merely recovery but a larger stock of financial claims priced on the assumption that future shocks would also be liquidity-bridgeable – shocks where underlying productive capacity remains intact and the constraint is purely temporal, bridgeable by income support and market liquidity until the real economy restarts. Asset prices recovered faster than the real economy, and the financial system emerged with a higher ratio of claims to underlying productive capacity and with the lesson embedded that shocks could be monetised. Shvets’s cushion is partly the residue of that lesson: the market has capitalised expected rescue capacity into current valuations, which means the cushion and the bubble are the same object viewed from different angles.

The rescue assumption has a load-bearing condition, however: the shock must be liquidity-bridgeable. The Strait of Hormuz has been effectively closed since late February, and the Houthi declaration of 8 June threatening a Red Sea blockade now puts the only significant maritime workaround under direct pressure – Saudi Arabia has been routing oil exports via the Red Sea because Hormuz is closed. Diplomatic talks are stalled, Iran and Israel exchanged missile fire on 7-8 June in the most serious test of the April ceasefire to date, and while both sides have conditionally stood down, the underlying conflict is unresolved. What is missing from this system is not liquidity but molecules – barrels that cannot move, feedstocks that cannot reach crackers, and LNG that cannot reach European and Asian industrial users. The standard objection that the world is less oil-dependent than in the 1970s mistakes where the dependence has migrated: from crude into gas and petrochemical feedstock reliance, while just-in-time logistics eliminated the inventory buffers that previously absorbed disruption across multiple production cycles. The current shock transmits not through the price channel but through a volume constraint propagating downstream through input-output chains, each exhausted buffer revealing the next, on no policy-determined timeline.

That physical constraint is also what makes the stagflation threat real rather than theoretical. The Survey of Professional Forecasters projects CPI at 6% for 2Q26, with May data due tomorrow and the FOMC meeting on 16-17 June – central banks facing energy-driven inflation cannot ease without risking re-anchoring inflation expectations upward, yet the real economy is slowing simultaneously. The fiscal side of the rescue is constrained too: global debt has reached a record $353 trillion, and the 2020-scale income replacement that converted a real-economy shutdown into a liquidity-supported financial order is not available at the same scale twice in 6-7 years.

The financial system the physical shock arrives into is already carrying the vulnerabilities that 2020 exposed and only partially resolved. Private credit sits on a large pool of assets without daily liquidity or transparent pricing, with the AI disruption of SaaS revenue streams now threatening the cash flows that justified the original lending. The AI hyperscaler story connects here because data centres run on the energy and feedstocks the Hormuz closure is restricting, and hyperscaler valuations are the primary weight in the current momentum trade. A correction there does not stay in equities – it travels through the collateral and leverage structures of structured credit markets, as a US housing correction travelled through mortgage-backed securities into the global banking system in 2008.

Three of the world’s largest sources of cross-border capital are withdrawing simultaneously through independent channels – Japanese repatriation as the Bank of Japan normalises policy, GCC sovereign wealth fund redirection as reduced hydrocarbon revenues compress the capital available for foreign deployment, and China’s structural reduction in long-end Treasury exposure – and the combination is tightening global financial conditions through channels that conventional monetary policy cannot offset.

The belief that this cycle is structurally different from the ones that ended badly is the standard argument at the top of every previous one. The bull case requires Iran and tariffs and China’s balance-sheet slowdown and the credit cycle and Japanese repatriation and GCC redirection and hyperscaler free cash flow to all turn at once across drivers that share no common factor. That is a wish list, not a scenario, and the burden of proof sits with those making it. The overdetermined downturn argument has not shortened – if anything it has lengthened.

King is right that timing is unknowable, and right that the momentum trade traps even those who see the fragility – one cannot prudently sit out while it continues. However, neither observation bears on whether there is a real cushion and the cushion Shvets identifies is nominal rather than real: a stock of claims contingent on the same conditions it is supposed to buffer against, backstopped by institutional rescue capacity that is narrower now than it was in 2020 and designed for a different kind of shock. The Chanticleer framing – the bubble ends through rate expectations and AI hubris – assumes a liquidity-bridgeable world. The question Friday’s session opened is whether this particular correction has that exit available to it. A 1970s comparison is a subject for another day, but the historical precedent for energy-driven stagflation meeting an over-leveraged financial system is not encouraging.