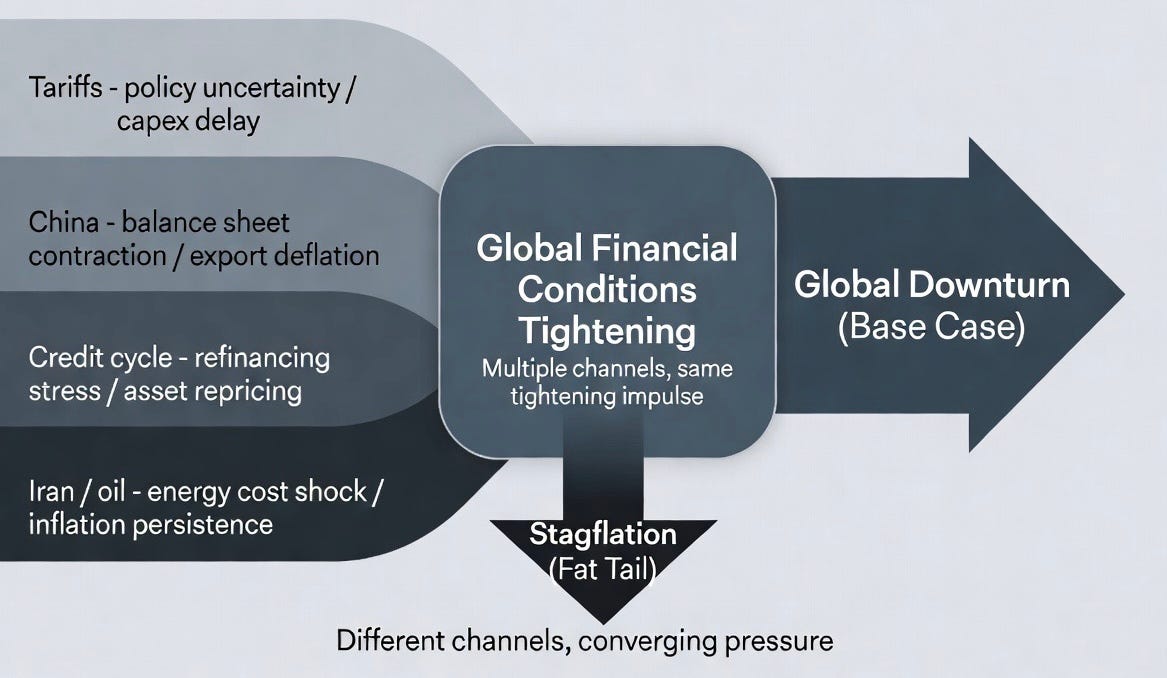

The Overdetermined Downturn

Iran, tariffs, China, and the credit cycle are converging – optimists on the global economy need all of them to resolve at once.

The case for a global downturn doesn’t rest on Iran, or on tariffs, or on China’s structural drag, or on where we are in the credit cycle. It rests on all of them simultaneously – and that’s precisely what makes it robust. When multiple independent causal chains all point to the same destination, the outcome is overdetermined: you don’t need every cause to fire, and knocking out one doesn’t rescue the bull case. The burden of proof sits with the optimists, and it’s a heavy one. They need everything to go right at once, across drivers that have nothing to do with each other. Calling that a bull case is generous. It’s more a wish list.

Resilience is a real thing, but it’s a buffer, not an immunity. It changes the timing and, in favourable circumstances, the depth – but not the direction, and that distinction matters less the further into the cycle you already are. Resilience arguments work against a single trigger; they have a shorter shelf life when multiple causes are already running.

Multiple causes, different channels

Start with tariffs. The trade uncertainty alone is sufficient to delay and distort business investment decisions and supply chains – the PMI data is already signalling it, with weaker new orders, softer expectations, and inventory mismatches pointing to behaviour adjusting in real time, and the transmission into corporate decision-making underway regardless of what happens in the Strait of Hormuz. Add China’s structural position: property sector deleveraging, weak domestic consumption, and export overcapacity exerting deflationary pressure across global manufacturing. That dynamic is self-sustaining and pre-dates the current conflict. Then layer in credit cycle position – rate tightening since 2022 is still working through the system, with commercial real estate stress, private credit vintage risk, and consumer credit deterioration visible across rate-sensitive economies.

These causes are not fully independent – they share transmission channels through trade flows, rates, and global liquidity – but they are not co-linear either. Tariffs operate through policy uncertainty and supply chain disruption; China’s slowdown is balance-sheet driven; the credit cycle reflects prior monetary tightening. They reinforce the same outcome through different mechanisms, which means the standard analytical move of identifying a common factor and discounting the rest doesn’t work here. Any one of them is a meaningful headwind. Running together, through different channels, they are a base case.

Iran is the accelerant, not the cause – which strengthens the base case confidence, because it means the downturn is overdetermined before the Middle East enters the calculation.

The oil price problem is structural, not transient

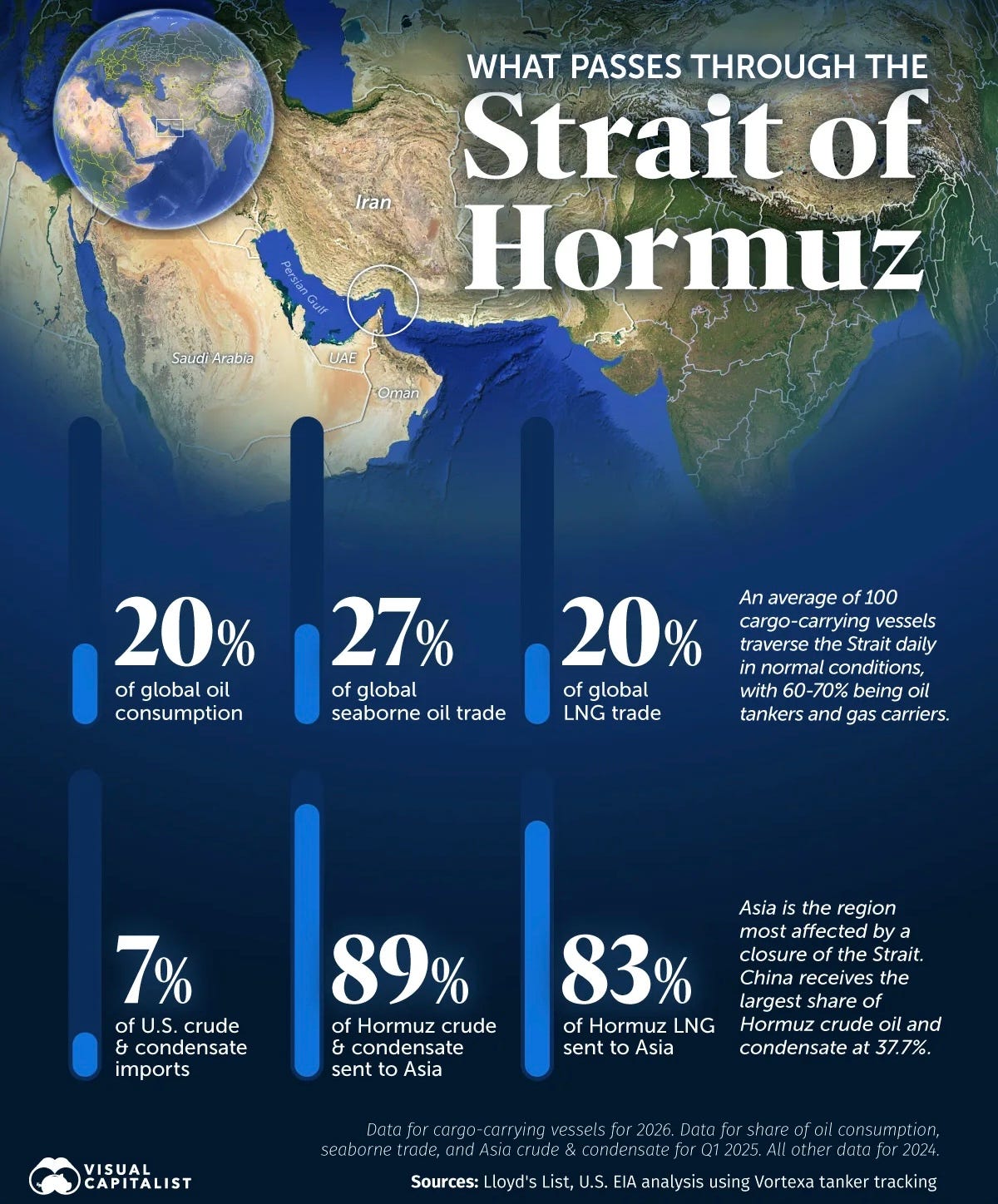

Even on an optimistic conflict timeline, a growing share of analyst forecasts now clusters sustained Brent well above prior baselines, with disruption scenarios pushing averages between $80 and $100 well into 2027. That is not a spike; it is a sustained cost input, and its implications for monetary policy are severe. The Federal Reserve’s post-2022 credibility rests on having broken inflation expectations. A persistent energy floor at that level forces a genuine dilemma: hold rates tight into a slowing economy, or ease and risk re-anchoring inflation expectations upward. Neither path is clean, and the usual assumption that the US is insulated by its more diversified energy mix doesn’t resolve a bind that operates through global commodity pricing and import costs regardless of domestic production.

The deeper problem is that sustained energy costs at this level are fiscally and financially corrosive well before they show up in headline CPI – they compress margins, strain household budgets, and force central banks into a reactive posture that leaves them perpetually behind.

The standard rebuttal – that the global economy is less oil-dependent than it was in the 1970s and therefore less exposed to an energy shock – misses where the dependence has migrated. The world substituted oil reliance with gas reliance, and LNG is now a critical feedstock for European and Asian industrial capacity. The Strait of Hormuz carries a substantial share of global LNG flows alongside oil. A disruption that looks modest against 1970s oil-shock metrics hits very differently when you account for what sustained LNG price elevation does to German manufacturing, South Korean power generation, and Japanese industrial input costs.

The Gulf capital flow channel is almost entirely missing from Western analysis

Gulf sovereign wealth funds and state investors are significant liquidity providers across global credit markets, real estate, infrastructure, and private equity. The conflict is already shifting their capital allocation calculus toward domestic priorities: reconstruction, expanded defence postures, and sovereign buffer-building pull capital inward.

The most visible early signal will likely be in private credit and infrastructure funds, where Gulf anchor commitments have underpinned deal flow – retrenchment there widens spreads and stalls projects well before any central bank moves. This doesn’t register in rate decisions or CPI prints, but it tightens financial conditions quietly and persistently across credit spreads and project financing in both emerging and developed markets. It is a shadow tightening channel, operating outside the standard monetary policy framework, and almost no current commentary is pricing it.

The ceasefire assumption is the weakest link in the optimistic scenario

The short resolution timeline that underpins the bullish case requires Iran to accept terms that its incentive structure actively resists. Iran has absorbed extraordinary costs before – the 1980s war with Iraq, maximum pressure sanctions, the collapse of the JCPOA – without capitulating to externally imposed conditions. The current situation reinforces that pattern: every month the conflict continues without achieving its stated objectives strengthens Iran’s deterrence posture for the next round and demonstrates the limits of the strike campaign. The incentives point toward endurance, not accommodation, and historical behaviour provides no basis for assuming otherwise.

The optimistic timeline is an assumption. The forecast label is a misnomer.

Bank capital deregulation adds fuel, not stability

The US move to ease bank capital requirements is framed as pro-growth stimulus, but the timing inverts its logic. Expanding credit supply at precisely the moment credit quality is deteriorating doesn’t resolve the underlying stress; instead, it distributes it into the banking system. The borrowers who fill the expanded capacity are those who need it most: leveraged real estate plays at late-cycle valuations, private credit roll-overs on assets marked above realistic exit prices, consumer credit extended into deteriorating household balance sheets. The collateral underpinning these loans is price-inflated; the macro outlook is worsening; and the loss, when it crystallises, does so 18 to 24 months out – after the origination decisions are made and the capital is deployed.

Meanwhile share buybacks, the other standard deployment channel for freed-up capital, are constrained by elevated equity valuations. The animal spirits the deregulation is designed to activate are unlikely to fire in the intended direction. What remains is credit expansion into a deteriorating cycle, with the reckoning deferred but not avoided.

Stagflation is the fat tail, not the base case – but the tail is thickening

The base case is downturn. Stagflation sits a step beyond it – not the most likely outcome, because the demand destruction from a slowdown is itself disinflationary. But sustained oil near $100, tariff-driven goods inflation, and compressed Gulf liquidity simultaneously narrow the standard escape routes. The inflationary pressure here operates on two tracks – cost-driven through energy and tariffs, and availability-driven through supply chain disruption and potential goods shortages. Both are inflationary; neither is responsive to demand-side policy tools. And neither is stabilising – the conflict continues, tariffs are still being layered, and supply chain stress is a lagging effect that hasn’t fully transmitted yet.

The usual relief valve – looser financial conditions, demand stimulus, falling energy costs — is partially closed. That’s what makes it a fat tail rather than a remote one: not the probability of entry, which is already elevated, but how narrow the exit routes become once you’re inside it – and how many of those routes are being closed by the same dynamics driving the downturn in the first place.

The pragmatic framework, then, is this. Downturn is base case – overdetermined by causes that are already running, through different channels, across different parts of the global economy. A deeper and longer version is the most plausible stress scenario. Stagflation is a tail, but a thickening one with fewer exits than the consensus models. The optimists need to beat all of that simultaneously, and the argument for doing so keeps running into the same problem: it requires a world in which almost nothing that is currently happening continues to happen. That’s a difficult case to make when the overdetermination is already visible in the data.

Going to be one hell of a ride