Two Spikes Coming?

Cushing is below operational minimum. The market hasn’t noticed. It will.

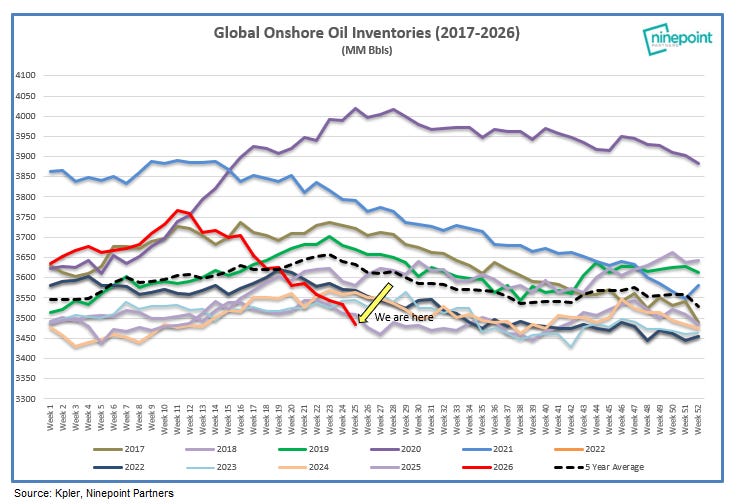

Cushing, Oklahoma is the pricing point for West Texas Intermediate (WTI) crude and the physical hub through which US oil supply flows to refineries across the Midwest and Gulf Coast. As of 25 June, inventories have fallen to 19 million barrels, below the operational minimum (~20mb) that the industry considers the threshold for physical stress. The US Strategic Petroleum Reserve (SPR) has fallen to 331.2 million barrels, the lowest since 1983. According to the IEA, global inventories are at their lowest seasonal point in recorded history.

The market has priced almost none of this.

What happens with Cushing below operational minimum?

When inventory falls below the operational limits (~20mb) – which Cushing has now breached, at 19mb – the hub enters a stress zone rather than hitting a cliff edge. The operational minimum is not a precise failure point; it is the threshold below which there is no buffer left to absorb further stress. The immediate effects are mechanical.

Pipelines that draw from Cushing operate on pressure differentials, but inventories at this level do not cause pipelines to fail instantaneously. What deteriorates first is scheduling reliability, the ability to guarantee volume and timing. Refineries that depend on Cushing lose the flexibility to absorb disruptions or respond to demand spikes. They are forced to draw on their own tank inventory as a buffer, but those buffers are also depleted.

Blending flexibility deteriorates with it, because the crude that remains at tank bottoms is the lowest quality and pulling it through creates blending problems. Cushing’s core function is blending different grades from the Permian, Bakken, and Canadian streams to meet pipeline quality specifications and refinery feedstock requirements. When you’re scraping the bottom, blending optionality narrows significantly, so refineries either accept degraded feedstock or reduce runs.

The financial effect then follows. WTI physically settles at Cushing, and when physical delivery becomes constrained, physical tightness increasingly dominates futures pricing. You get extreme backwardation and basis blowouts as buyers scramble for physical barrels that can’t be reliably delivered. The WTI-Brent spread would likely widen – the US price and the global price decouple – and with US export capacity under pressure, nothing is left to hold Brent down.

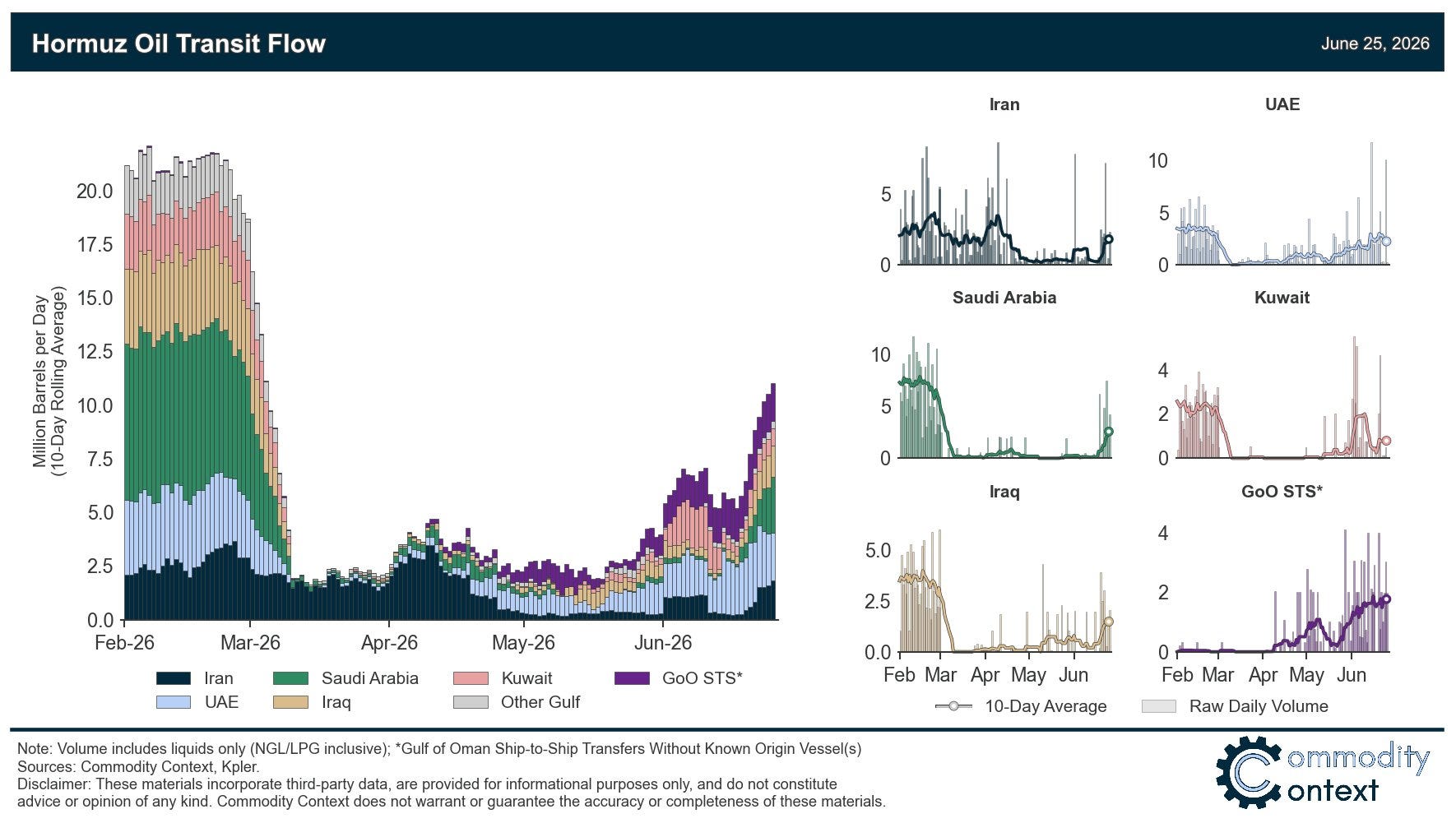

Midwest refineries are the most exposed because they are dependent on pipelines from Cushing and have limited alternative supply access. Gulf Coast refineries theoretically have more flexibility as they can draw waterborne imports, but they are already running at record utilisation. US crude exports have run at record levels since March, with the Gulf Coast processing additional crude to produce the diesel, jet fuel, and gasoline that Middle Eastern and Asian refineries could no longer supply at normal volumes as Gulf feedstock flows through Hormuz collapsed. That additional throughput has been draining Cushing. The crude draw and the product export are the same event viewed from different ends of the supply chain.

The broader consequence is that Cushing operational stress would convert a global supply disruption into a US domestic supply disruption simultaneously. The US has been acting as supplier of last resort to the world because its own inventory position appeared comfortable. Once Cushing signals stress, that export capacity comes under pressure because domestic refinery supply tightens. The price signal that has been suppressed by reserve draws then has to clear through the crude price instead, spiking rapidly.

That is the first spike.

The second follows when the global restocking wave arrives. Most major economies have been drawing strategic reserves throughout this crisis – the IEA coordinated a 400 million barrel release across member nations, Japan and South Korea have drawn their modest reserves steadily, and Europe has done the same to varying degrees. China’s position is opaque – Beijing does not publish reserve levels transparently – but the working assumption is that Chinese reserves have also been drawing to keep refineries running through the Hormuz disruption, given that China normally takes roughly 20% of Gulf crude and its total imports are well down.

When those draws exhaust, every country needs to restock simultaneously. They will all be competing for the same barrels at the same moment, in a market where Hormuz throughput remains well below pre-war levels and the reconstitution sequence – demining, tanker repositioning, hull fouling, refinery feedstock switching – has barely begun. Reopening is not restoration, but the market continues to treat it as though it were.

The shape of the financial fallout is therefore probably two distinct repricing events rather than one continuous move. The market has been reactive and consistently wrong in the dovish direction throughout this crisis. It priced the Islamabad MOU as restoration. It priced the 70-vessel day on June 24 as recovery, when it was just clearing the stranded queue backlog. It will price the first spike as the peak. Then the restocking demand will appear and the market will price that shortage separately, when it can no longer be ignored.

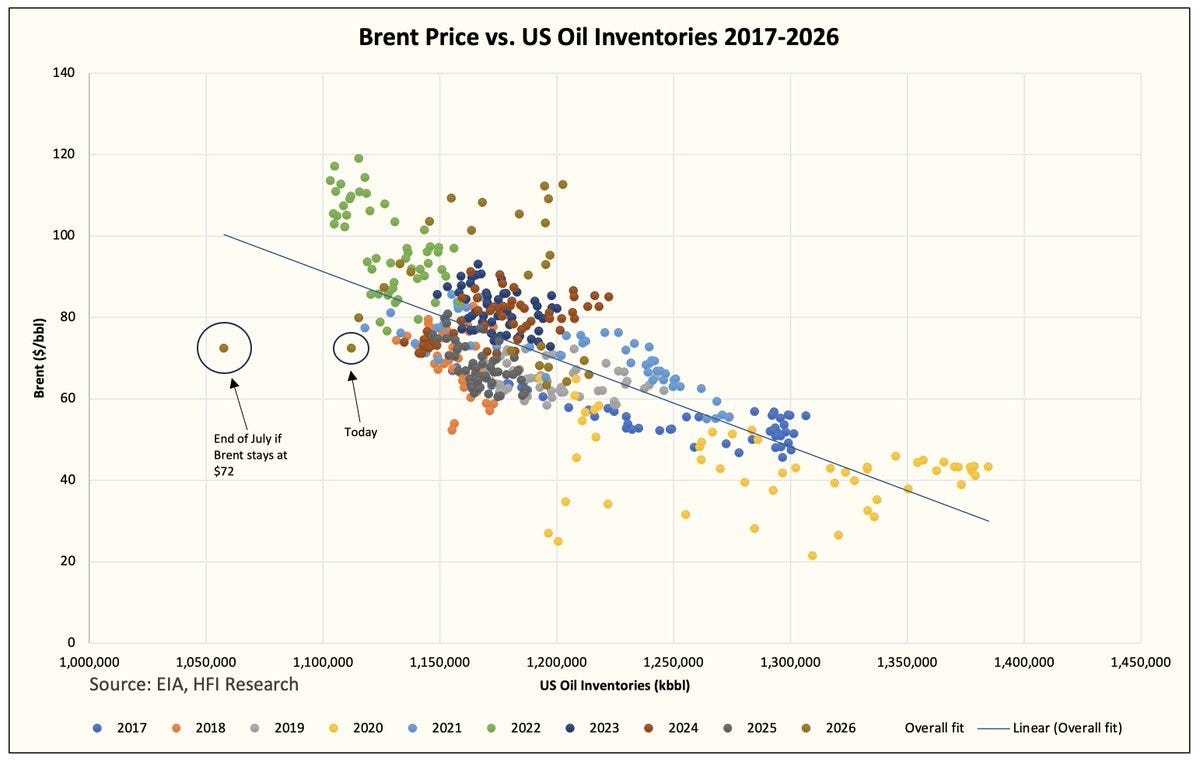

Two spikes. Two moments of forced repricing, each preceded by the same premature relief. Brent at $70 tells you the market thinks the crisis is over. But it isn’t. Brent at $70 instead tells you the market hasn’t looked at what comes next.

Cushing at 19 million barrels and a $0.55 front spread can't both be right. The spread says supply is meeting demand. The delivery point says there's nothing left to deliver. The reason both numbers exist at the same time is that the spread reflects the national aggregate and the stress is at the physical hub. The spread can stay flat while the delivery point breaches operational minimum, right up until the scheduling failures and blending problems at Cushing get large enough to force the national number to move. That move won't be gradual.

The two-spike structure is what most people will miss because the market is pricing one event: Hormuz reopens, relief arrives, crisis over. It hasn't priced what happens when every country that drained reserves during the crisis needs to restock at the same time, competing for the same barrels, through a Strait that's still operating below pre-war capacity because demining, tanker repositioning, and refinery switching take physical time no signature can compress. The relief rally is pricing the headline. The restocking wave is the second bill, and nobody has budgeted for it yet.

And the trading algorithms react only to headlines. Not to the real world.