Ending the War on Paper

The MOU removed the war premium from oil while leaving the deficit premium untouched – the deal changes the size of the wave still to come, not whether it arrives

The market sold the war premium out of oil within a week of the Islamabad Memorandum of Understanding (MOU), and it was logical to do so. Brent fell from the low $90s to the mid $70s, giving back nearly all the gains accumulated since the conflict began on 28 February, on the reasonable judgement that a signed deal and a lifted US naval blockade would open the Strait of Hormuz and get barrels moving again. The premium for that risk should fall on a credible de-escalation signal, and it has.

This is a complex issue, however, with multiple moving parts, and the market’s error lies in what it has also priced. Oil has faced two premiums since March, but the market has treated them as one and removed too much. The war premium has gone, correctly, but the deficit premium has not – nothing in the MOU increases the volume of oil moving through Hormuz today. Global consumption has run ahead of production for months, the gap covered by drawing down strategic and commercial inventories rather than by replacing lost supply, and a signed deal does not address that – only a return of physical flow does. The forward curve confirms the distinction that the spot price recognises and the market has blurred: Brent is still in backwardation, the signature of a physically tight market, rather than flattening as it would if supply had actually loosened. The paper market has moved lower yet the physical market has not followed it.

That gap will close eventually, and the size of that mispricing gap is what this piece calls the wave: not a new shock, but the delayed recognition of conditions already in place. As argued since April, what the Strait’s closure produced was a hydrocarbon shock rather than just an oil price shock, and the market still does not acknowledge that the two behave differently, which has downstream implications. An oil price shock moves along the supply and demand curve, whereas a hydrocarbon shock operates on two tracks simultaneously. The price track is familiar – energy costs rise, producing a dilemma for central banks. The physical track is the one the market has not priced: the closure restricted the supply of industrial feedstocks – naphtha, LNG, helium, chemical intermediates – that underpin global supply chains with limited substitutes. That restriction does not respond to price signals because it is a volume problem rather than a cost problem. Higher prices do not produce more molecules. The wave, when it arrives, will reflect both tracks – not just the crude price, but the downstream cost of months of petrochemical feedstock disruption working its way through input-output chains that have already exhausted their buffers.

Reopening is not restoration

The political picture is as contested and unclear as the physical one. Washington claimed the Strait was open, but Iran announced a fresh closure on 20 June in response to continued Israeli strikes in Lebanon; CENTCOM denied that control had changed and stated that 55 merchant ships had transited that day. All three are official pronouncements, but should be read cautiously.

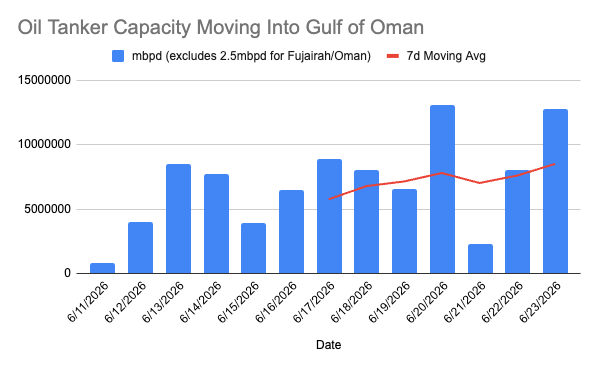

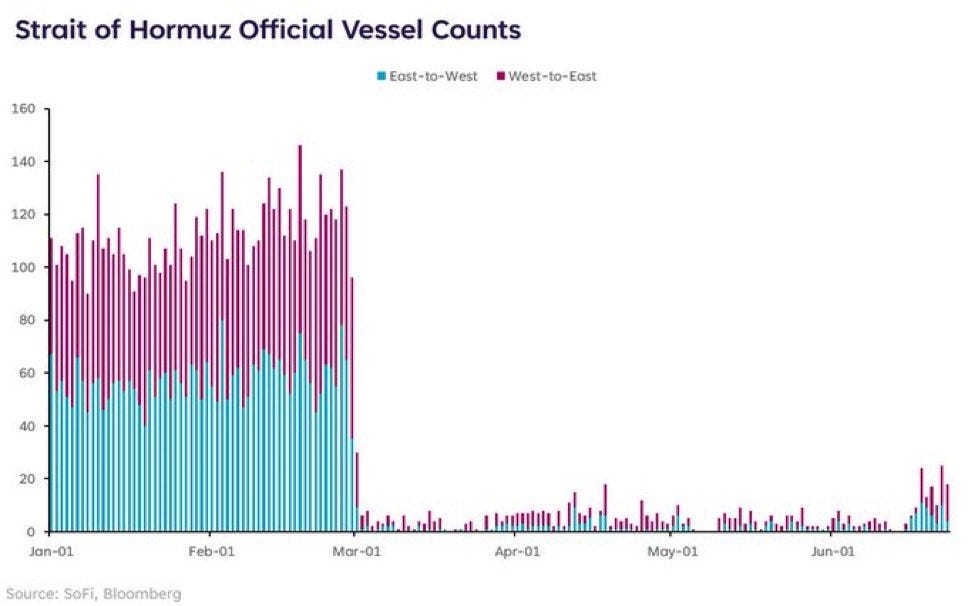

Independent vessel-tracking data is a more reliable anchor than political statements. Transits are well below pre-war levels given the Strait is only just beginning to open. Implied flow has slowly ticked up to a 7-day moving average of 8.5 mb/d by 23 June against a pre-war level of around 20-21 mb/d, roughly 40% of normal. Prior to the war, the Strait averaged around 125 vessel crossings per day; this collapsed to single digits from late February. Kpler reported 71 transits over 19-21 June with a weekend peak of 35 on 20 June, and 39 on Monday 23 June. The initial surge reflects pre-positioned vessels clearing – laden tankers that needed only political clearance to move – rather than a restored loading and shipping cycle. Empty tankers returning for new cargoes are not yet visible in the data.

Reconstituting the tanker fleet could take eight to ten weeks before meaningful new supply reaches its destination. Part of the fleet that serviced the Middle East-Asia route has spent more than three months redeployed onto longer routes. Vessels that spent months at anchor have accumulated hull fouling that reduces speed, and the attention they need will compete for drydock capacity with ships requiring war-damage repairs and insurance surveys. Demining in the Gulf remains a work in progress, and shipowners continue to exercise caution in the uncertain environment amid still-elevated insurance premiums.

Mark Lashier, Chief Executive of Phillips 66, explained the next constraint: between 90 and 100 million barrels remain trapped in the Strait, clearing only as fast as onshore storage can receive them. “Most of the tanks on shore are full before crude can appreciably ramp up,” he said. In other words the bottleneck is storage, not the waterway. And even when tanks drain, Asian refineries that spent months running mismatched alternative feedstocks – US light tight oil, West African crude, Russian Urals – do not switch back to Gulf sour crude instantaneously. They need to variously clear feedstock inventories, renegotiate term contracts, physically adjust crude slates, ramp-up production, and manage deferred maintenance. Thus the sequence from an open waterway to lower fuel prices faces at least three transitions – waterway to storage, storage to refinery, refinery to product – each with its own lag. Lashier’s conclusion: “There’s going to be some structural shift in what the crude floor is”.

The shortfall from disrupted Gulf exports was roughly 11-13 million barrels a day at its peak. Before the war the Strait carried around 20% of global petroleum liquids, roughly a quarter of seaborne oil trade and around a fifth of global LNG trade on top of that. The IEA puts full production restoration at January 2027, while ADNOC’s Group Chief Executive Sultan Ahmed Al Jaber estimated flows at 80% of pre-war levels no earlier than four months from an effective agreement. That suggests around November 2026, with full normalisation not expected until Q1-Q2 2027. US shale or other alternative sources cannot fill the gap. Output has barely moved from its pre-war level, and energy companies are unlikely to make the necessary long-term investment commitments in such uncertainty. Further, equipment and workforce reductions from the pre-war low-price period cannot be reversed quickly, and new production takes six to twelve months to crystallise.

Buffers and China

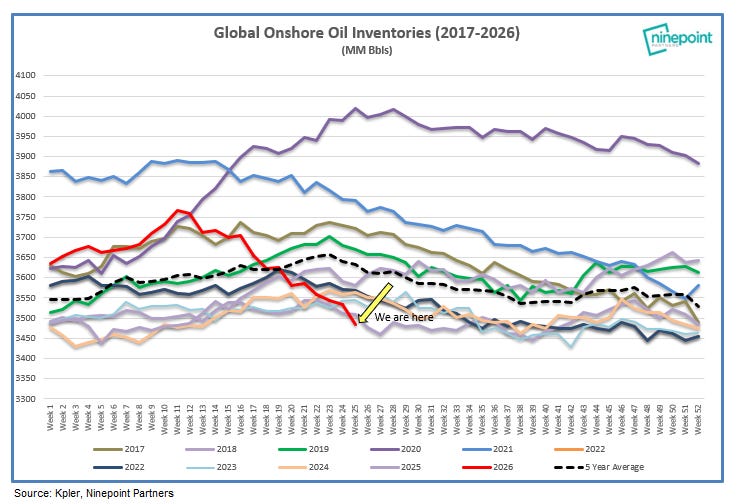

Strategic reserve and commercial inventory drawdowns have absorbed the supply shock, but only temporarily. Even on a clean and rapid reopening of the Strait, reserve draws will slow before both production and shipping flows have returned to pre-war levels. The lag between those two conditions could run to months, reflecting bottlenecks in storage and at refineries. There are several difficulties in forecasting the length and size of this lag. There is the production side, discussed above, and also the impact of strategic reserves given lack of past experience to draw on. This reflects determination of the appropriate floor, at which point drawdowns cease, and the timing and speed at which governments seek to replenish reserves. These aspects have the potential to turn what was a counter-cyclical buffer into a pro-cyclical one. The observed price fall that followed the MOU is exactly the signal that brings suppressed demand back to the spot market. David Fishman of the Lantau Group set it out explicitly: “The thing that can’t be sustained forever is the stockpiles of crude. If prices weakened, you’d expect the first thing they do is start to stockpile again.” Returning demand will hit the market at the same moment the IEA’s coordinated 400 million barrel emergency release is set to taper to zero by October, and commercial storage, including at Cushing, is already drawing toward operational floors last tested in 1983.

The bulk of the 2026 US SPR releases have been structured as exchanges rather than sales – barrels out immediately, barrels back under contract – so Washington is not an immediate net open-market buyer. That said, Trump has stated he retains the option of “resetting the clock” if he believes Iran is “not complying”, which would require immediate reserve rebuilding. However, the 60-day window is too short to restore that buffer to a level that would provide meaningful leverage, making the reset option less available than it sounds, and suggesting a binary outcome – either a rapid rebuild or a delayed one, with dramatically different price implications. The same is not true elsewhere, though. Japan, South Korea, and Europe contributed substantial volumes to the IEA release from industry obligation stocks and face a mandatory open-market rebuild.

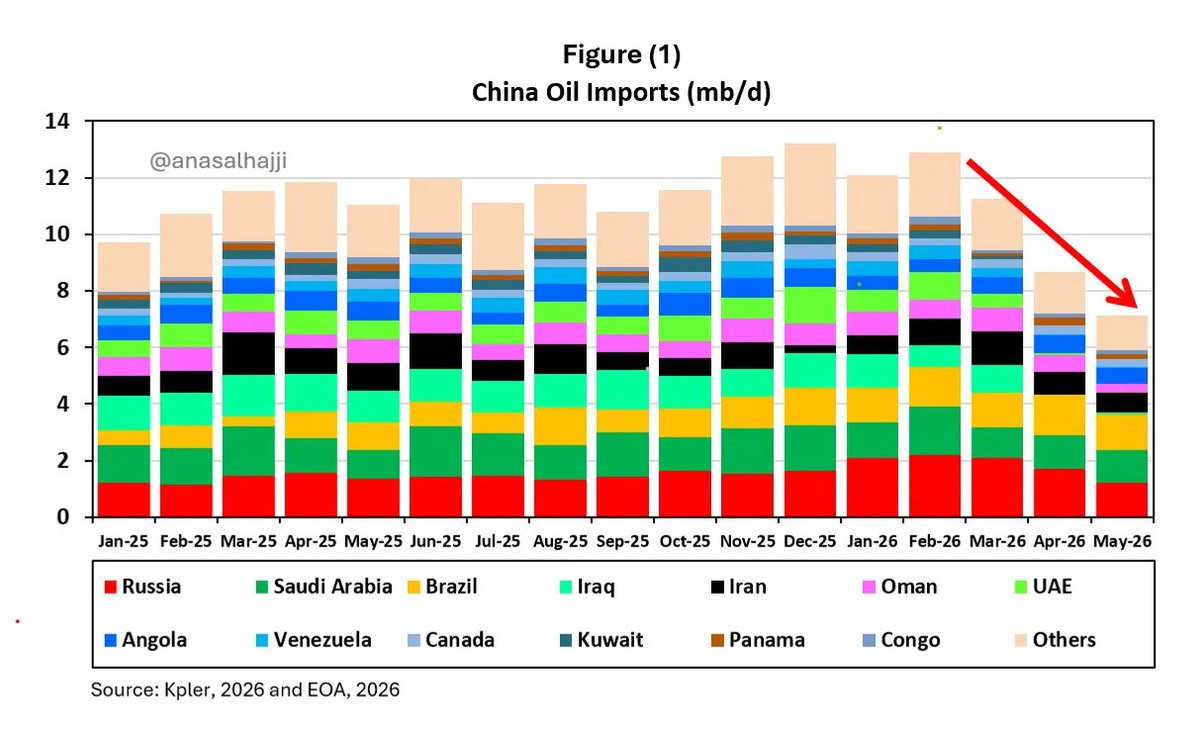

Suppressed Chinese demand has eased the shock during the closure but now compounds the recovery problem. Societe Generale analysts described China as “the invisible hand that is rebalancing the market,” estimating it curbed oil imports by around 3 mb/d – an amount nearly equal to Japan’s total crude demand – by drawing down onshore stockpiles and limiting refined product exports rather than competing for scarce seaborne barrels. China’s centrality to the crude price now creates a modelling problem that was not foreseen. The traditional price variables – US SPR levels, EIA inventory data, Cushing stocks, rig counts – were designed for a market where the US was the marginal consumer and the marginal reserve manager. China has taken both roles, through import volumes that can swing by 3 mb/d and massive combined strategic and commercial reserves estimated at 1.2 billion barrels.

Compounding the forecasting challenge is the distinction between the operational floor and the political floor. The operational floor is the engineering minimum below which tank farms and pipelines cease to function. The political floor is the level at which a government intervenes to stop further draws, and it lies above the operational floor by a margin that varies with political circumstances but is never published. For the US, Trump’s admission at the G7 that reserves would run out in “about four weeks” was a rare public signal of where the political floor lies.

Everything about China’s strategic reserve is opaque – size, operational floor, political floor – as its management is a sovereign policy instrument rather than a reportable obligation. Unlike the US SPR, it has no exchange mechanism, so its rebuild will be a sovereign purchasing decision. It will have an internal threshold – the political floor – below which stockpiles cannot fall, so China’s re-entry into the spot market is driven by that threshold, and the timing cannot be inferred from price data alone. Yet it also has an established pattern of aggressive accumulation whenever prices fall and many of the tankers now leaving the Gulf are carrying Iranian crude made available by the sanctions waiver, and most appear headed for China – the buyer that has absorbed the bulk of sanctioned Iranian oil and has a strong incentive to restock at current prices. Hence, the market is pricing a recovery whose two largest demand variables – the scale and timing of Chinese re-accumulation – are determined by political decisions that are invisible from outside.

Supply glut?

Despite the turmoil the IEA has returned to its oil glut prediction. Its June OMR forecast a 4.7 mb/d oversupply in 2027 and this deserves the same scrutiny as its January 2026 forecast of a comfortable 2026 surplus. That rested on undisturbed supply and was overtaken by events within eight weeks of publication. The June projection rests on an equally optimistic restoration assumption. The IEA’s own May OMR said rebuilding the cumulative 900 mb stock deficit would require an extra 1 mb/d of supply for three years on top of underlying demand growth; the EIA’s June STEO assumes flows resume in Q3 but full trade-pattern restoration not before early 2027, in line with ADNOC and the IEA’s own assumptions. There will be a surplus eventually, but the question is whether it occurs before or after the demand recovery and reserve rebuild push prices higher in the fourth quarter. The sequencing outlined above suggests later rather than sooner.

The wave

The MOU does lower the ceiling of what the wave might have reached. The market had consistently refused to price the worst case – a Strait that stays shut well into the second half of the year – and the MOU removes that tail risk, which is why the war premium came off correctly. But the market has gone further, pricing as though the supply shortfall itself has cleared, and it has not. The floor is set by the physical reconstitution lag, not by the diplomatic calendar. The wave arrives smaller than it would have under continued escalation, because the ceiling is lower; it arrives larger than the current price allows, because the floor has not moved.

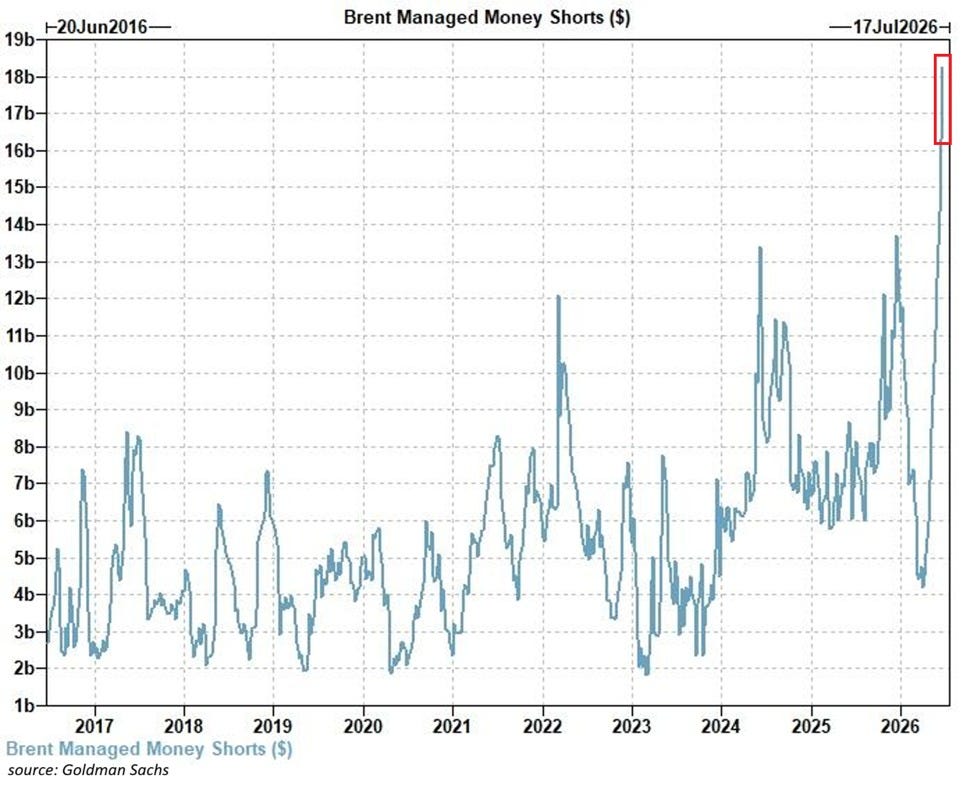

Brent managed money short positions have reached an all-time record, according to Goldman Sachs data – above $16 billion as of mid-June, well beyond the prior peaks of 2022 and 2024. When the physical data establishes what the financial positioning has denied, short-covering will become a second amplifier, accelerating the upward price move.

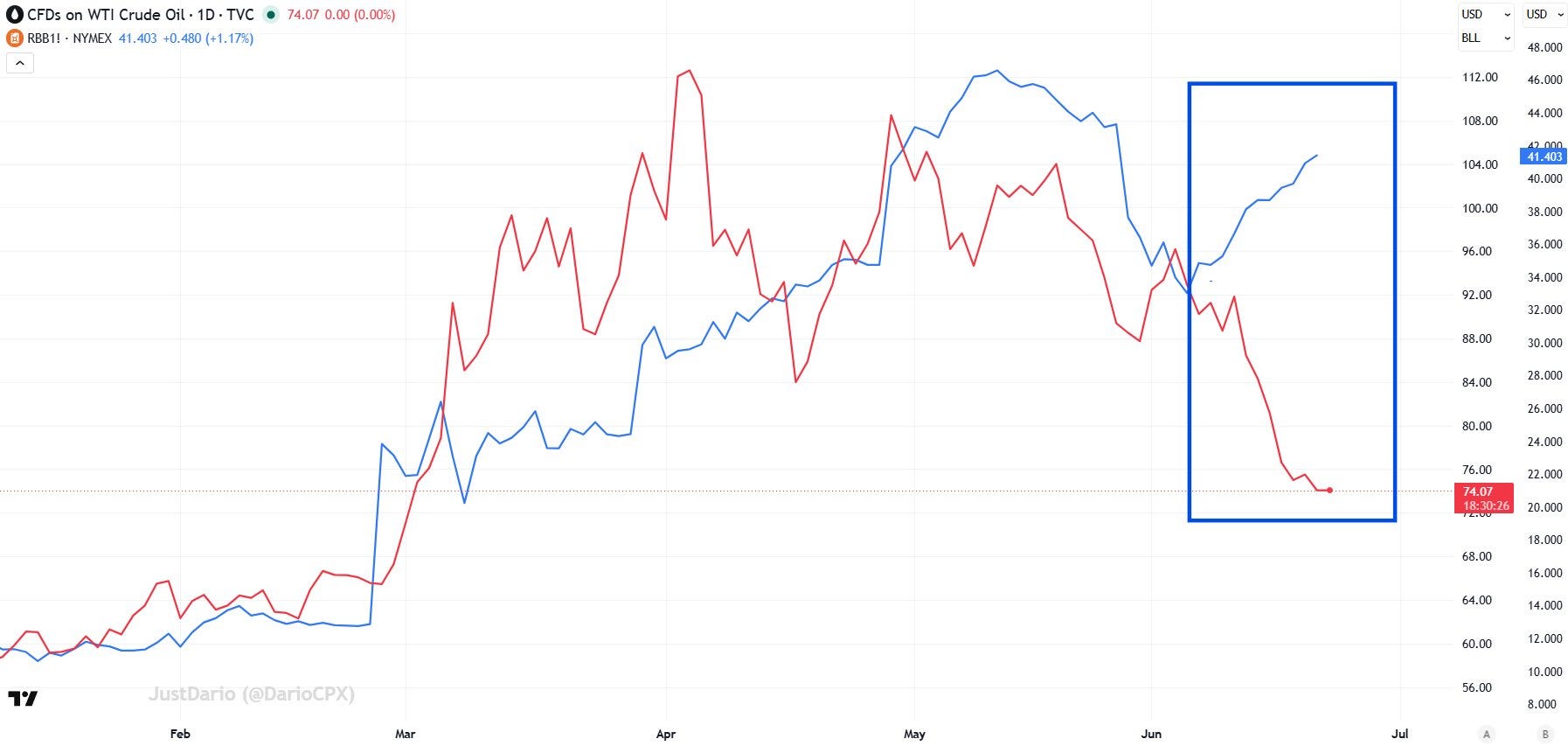

Crack spreads – the refinery margin between crude input and refined product output – have widened sharply into the falling crude price, with RBOB gasoline futures rising as WTI has fallen since the MOU. That divergence illustrates the two-track argument in real time: the crude price is being pushed lower by financial positioning while physical product markets are experiencing supply shortfalls. A market that has correctly priced a supply recovery produces stable or narrowing crack spreads, not widening ones. The spreads confirm that downstream physical tightness persists even as the headline crude price suggests it does not.

Whether the deal survives

The viability and longevity of the deal itself remains unsettled – the pattern of the first week echoing the observed reality of recent months.

Iran announced a fresh Hormuz closure on 20 June in response to continued Israeli strikes in Lebanon, and the Iranian delegation appeared to pull back from the Switzerland talks the following day, but the talks proceeded, concluding on 22 June with Iran’s Foreign Minister describing “major progress”. The talks also produced a communications line to manage Hormuz incidents. Iran and Oman subsequently formed a joint committee on Strait administration – an institution that reinforces Ghalibaf’s claim, in Iranian state-media remarks on his flight from Switzerland, that the Strait would never return to its pre-war situation. If that is even partly correct, the deal has not resolved the Strait question so much as deferred the dispute over who controls practical access to it.

The US Treasury issued a 60-day sanctions licence allowing the production, delivery, and sale of Iranian oil at market prices – a genuine concession clearing the path for Iranian crude to return to market at full price. Ghalibaf confirmed an agreement to release $12 billion in frozen assets, though the conditions remain disputed: Vance said the funds would require Qatar and US oversight and be restricted to US agricultural purchases; Iran’s central bank governor said Iran had no such obligation. Qatar and Pakistan confirmed a High Level Committee, four working groups, a communications line for Hormuz, and a de-confliction cell for Lebanon – the last of which Pezeshkian presented as a victory, saying the US had “been compelled to retreat on the issue of Lebanon”. Notably, the MOU contains no requirement for Iran to limit its missile programme; Trump stated at the G7 that “missiles aren’t the problem”, dropping one of the war’s many stated justifications.

The nuclear inspectors question shows how far apart the two sides remain. Vance claimed Iran had agreed to invite IAEA inspectors back, but Iran’s foreign ministry said it had made “no new commitments”. Trump then posted that Iran had agreed to inspections “long into the future”, adding that without this concession “there would be no further negotiations” – a public ultimatum delivered while technical talks were still under way. Vance led the Switzerland talks while Trump simultaneously threatened renewed strikes if Hezbollah kept attacking Israel, warned Iran’s leaders they “won’t even make it back” to their country if Hormuz closed again, and proposed imposing US tolls on the Strait after the 60-day period. Ian Bremmer, president of Eurasia Group, has argued on X that Vance says nothing on Iran or Israel that Trump does not want said – which would make the contradiction deliberate rather than chaotic, a good-cop/bad-cop posture that preserves Trump’s option to collapse the deal while Vance builds it. Whether Bremmer’s interpretation is correct or not, Iran is negotiating with a counterparty whose principals are saying opposite things in public, and the deal’s durability depends on which of them is actually setting policy.

The Lebanon ceasefire has largely held since the talks, though Israel has explicitly reserved the right to continue operations and has not withdrawn from southern Lebanon. Iran’s blocking condition – that other provisions of the memorandum will not enter the implementation phase until the war in Lebanon ends – remains formally on the record, and has not been met.

Outlook uncertain on magnitude, not direction

The 60-day period covers three partially overlapping things – the negotiating window for a final agreement, the Treasury sanctions licence, and Trump’s stated reset option if the deal collapses – that face the same precondition Washington may not be able to deliver, an end to the Lebanon conflict. A collapse of the deal would put the war premium back on top of a deficit premium the market has already mispriced. A reminder that the original JCPOA took nearly two years of intense negotiations and there there are fewer than 60 days left in this window. This deal is really another ceasefire extension, with all the uncertainty that entails both during the window and after it closes.

Upward pressure holds regardless of the diplomatic calendar, because of the gap between paper and physical reality. A further price rise into the third or fourth quarter does not need Iran to renege or Lebanon to reignite the wider war – it needs only the lag to hold, and the shipping and production data confirm that it should. Whether or not the deal survives, demand recovery will arrive before supply recovery, with storage buffers already drawn close to their floors, and all buyers competing in the same constrained market at the same time. Mohamed El-Erian, President of Queens’ College, Cambridge, and former CEO of PIMCO, writing days after the signing, set out the operational complexity – Hormuz does not reopen at the flick of a switch, given the insurance, demining, and production ramp involved – but his caution stays qualitative where the constraint is quantitative and timed.

The Islamabad MOU removed the war premium from oil while leaving the deficit premium untouched. The deal changes the size of the wave still to come, not whether it arrives.

The remaining five channels – the Gulf’s confidence economy, three simultaneous capital withdrawals from the US asset ecosystem, the US security commitment to Taiwan, Europe’s rearmament against a guarantee that is retrenching, and the AI capital expenditure cycle – will be addressed in follow-up pieces.

Apologies for the delay in publishing. The scene has been moving across multiple theatres simultaneously, and calibrating it has taken longer than normal.

Interesting article. Thank you. You don’t spend a lot of time talking about demand destruction. In Australia, the latest monthly government figures for the sale of petrol indicates a 7% decline compared to the same month in 2025. Many people have reportedly bought EVs and many more will not have received the ones they’ve ordered yet so I would guess that 7% is just the start. With increases in oil supply (from Iran and elsewhere) this isn’t great news for either the Gulf States or for service station owners.