Local Glut, Global Headline

Why a corridor between the Gulf and China is being mistaken for the whole market

Markets can be wrong for longer than seems logical. Yet if Hormuz reopens and Gulf production returns faster than assumed here, or if Chinese demand stays subdued for longer, then prices will remain low and the market will have been proven correct.

This piece isn’t a forecast of where oil prices are heading. Instead, it is an argument about how the market has reached its current conclusion, and why that interpretation is incorrect. Ultimately I may end up wrong about where prices go. However, even if I am, while the market simply chooses to ignore what the fundamentals actually show, I would prefer my error to be for a reason that was demonstrably clear and logical.

The market’s “global glut” argument mistakes a localised bottleneck for a global condition, then treats the price fall that it has caused as confirmation.

Two finite mechanisms are pushing prices down: coordinated strategic reserve drawdowns, and the clearing of the Gulf’s wartime backlog. Both are one-off and both are draining.

UAE and Iraq heavily discounted the trapped oil that exited the Gulf to clear the backlog, and China’s teapots opportunistically bought it cheap. Iran didn’t match that temporary discount, leaving its unsold oil floating at sea while it focused on longer-term buyers.

The pattern of a localised, rather than a global, glut is visible across West African crude too. Those prices have fallen unevenly, rather than in lockstep, reflecting a single mechanism unwinding rather than a global surplus.

A global surplus should broaden across grades and regions, and eventually ease product markets too. What we are seeing instead is concentrated distress in the grades and routes tied most closely to China’s absence and the Gulf backlog.

OPEC output in June remained roughly a quarter below February levels, and US crude inventories are near a multi-decade low. That fits a one-off backlog clearance pushing the price down worldwide while the underlying position stays tight – not a global surplus in the making.

I set out the local-versus-global distinction in detail in Reading the Spread – a price fall can come from a global surplus or from a bottleneck at one point in the chain, and the two are hard to tell apart on a spread screen. This piece updates that argument with what’s happened since.

OPEC output rose 2.34 million barrels a day (mb/d) in June to 18.75 mb/d according to Bloomberg’s survey – still 28% below February once the UAE’s exit from OPEC is factored in. Reuters puts June output higher, at 19.43 mb/d on the same post-UAE basis; measured against Bloomberg’s implied February base, that would make the shortfall closer to 25%. That’s a minor difference in method rather than a disagreement about direction, and both show output well short of pre-war levels.

A local supply problem can still move the global oil price, because the barrels involved are priced into the same global benchmarks everyone watches. However, Brent falling doesn’t indicate whether the fall is local or global. The pertinent question is what is driving it.

For years, Iran’s discount to Brent has really been a sanctions tax, not a market price. Teapot refiners – China’s small independent refineries mostly based around Shandong – often demanded $8-15 off Brent to compensate for the risk of buying sanctioned oil through shadow-fleet, non-dollar routes. The US Treasury’s General License X temporarily removed much of that risk, until 21 August. As a result, Iran’s discount narrowed to just $3 – closer to a normal quality discount rather than a risk discount – at exactly the same time the Gulf’s own discount was widening to clear its backlog. Thus, for a short time, Iran ended up looking more expensive than sellers who had no choice but to discount harder.

TotalEnergies chief executive Patrick Pouyanné commented that Gulf producers are “desperate to sell” crude they built up during the war. However, they face difficulty getting tankers through Hormuz because many shipowners remain unwilling to take the risk, hence producers have been forced to discount heavily to move oil regardless. He expects the market to take three to four months to rebalance.

Iran didn’t cut its price to match the discounted crude, but that’s not really because of stubbornness or inability. Rather, matching a discount that only exists because the Gulf has to clear a backlog would mean setting a low reference price Iran would then have to raise again once that backlog clears – this would look like backtracking to any buyer signing a longer contract in the meantime. Iran appears to be using the 60-day window to test and rebuild longer-term buyer relationships while dollar settlement is temporarily authorised, rather than winning a short-lived price fight it would later have to reverse.

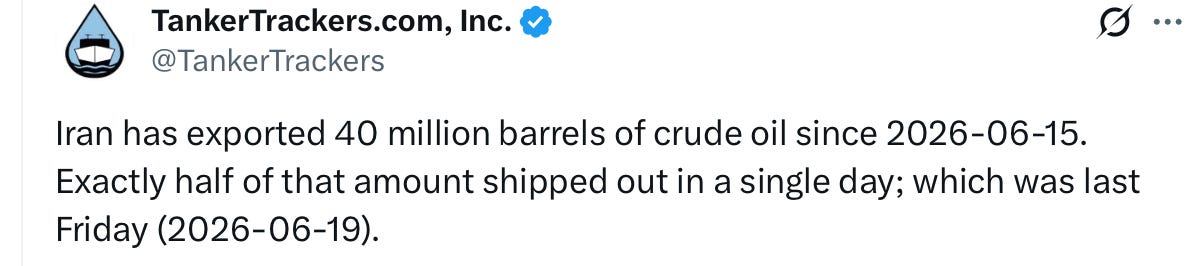

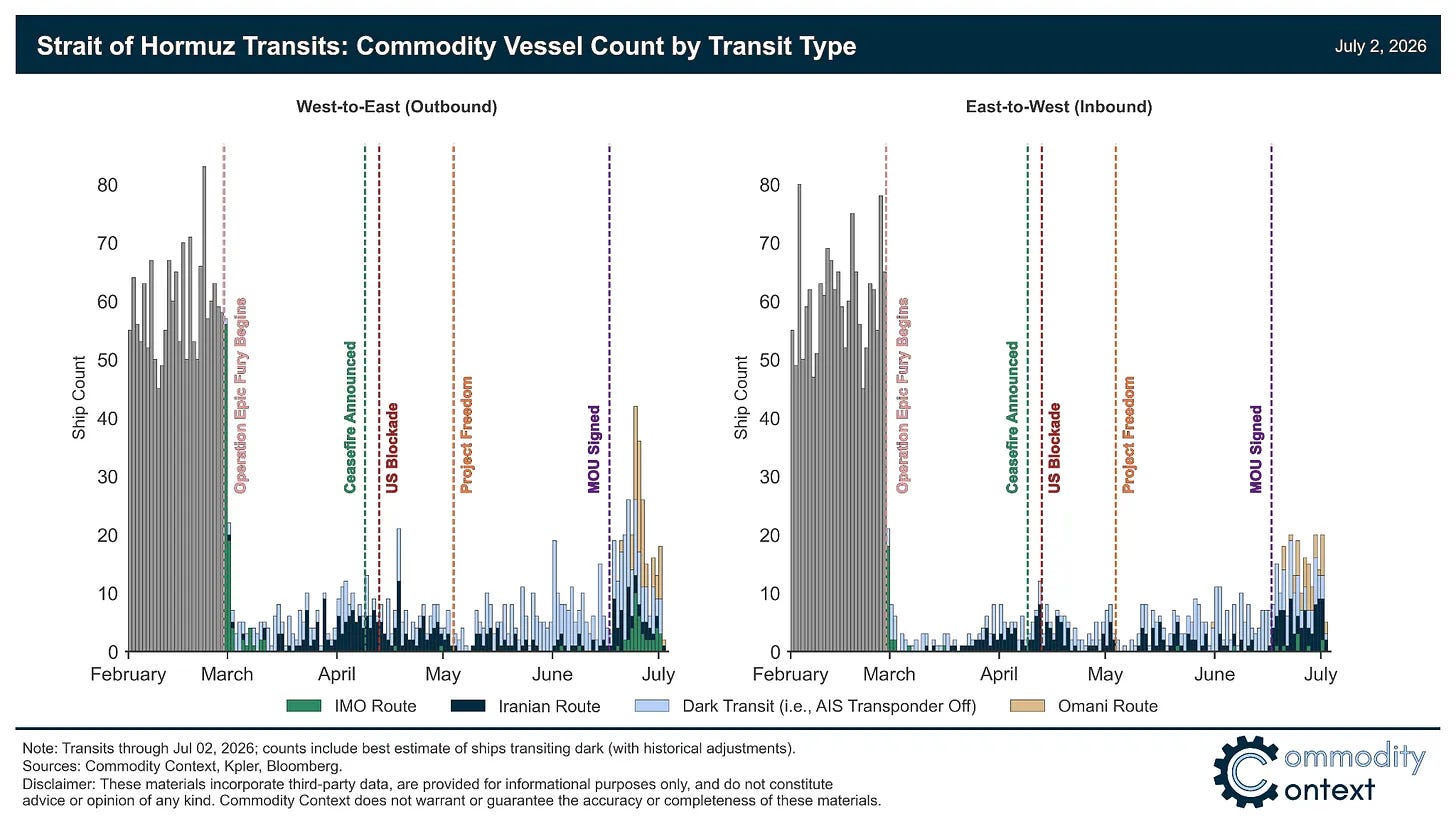

The result has shown up in the level of Iran’s oil on the water, the shipping industry’s term for crude that’s loaded and at sea but not yet delivered. It has risen to 58-68 mb, according to Vortexa, with more than 20 mb idling in Asian waters for at least a week and over 90% of cargoes showing no confirmed destination.

Most of that ostensibly stranded oil looks deliberate rather than accidental. TankerTrackers recorded roughly 20 mb leaving Iran in a single day on 19 June. Historically, Iran’s exports to China have been around 1.4 mb/d, with reported short-period peaks around 2.2 mb/d. So this single convoy was the equivalent of nine to fourteen days of Iran’s normal sales to China. That looks less like normal spot selling than pre-positioning: either for pre-arranged buyers, for floating storage near Asia, or for optionality ahead of another possible disruption. This fits the earlier point made in Better Flows more reasonably than an account of Iran being caught out by the market. Iran was positioning ahead of a possible new closure of the strait, not caught out by a market it didn’t see coming.

Oil from West Africa tells the same argument from a different angle, and although the pattern isn’t identical for every producer, it illustrates the mechanism described above for the Gulf-China corridor rather than a separate one. During the shortage, Asian refiners paid a premium for West African crude because Gulf oil wasn’t reaching them – any barrel that roughly matched their refineries would do, even at a high price and a less-than-ideal grade. However, with a sudden return of cheap Gulf oil, that premium had no reason to continue for barrels that were only ever a stopgap. Congo and Angola swung most from premium to discount. Congo’s Djeno crude went from a steep discount before the war to a premium during the shortage, and back to a record discount now – S&P had it at $11.86 below Brent on 26 June, and a July cargo offered at $14 below Brent found no buyer at all. Angola followed much the same path: Cabinda and Clov traded $10-15 above Brent in April, and by late June, Dalia, Pazflor and Hungo were selling at their lowest prices on record, with some cargoes offered close to $9 below Brent. Nigeria has moved in the same direction, but by smaller amounts: Bonny Light and Qua Iboe also spiked more than $10 above Brent during the shortage, and have fallen back to modest premiums of $2-3. Nigerian grades are more broadly useful outside Asia and were never bought purely as a stopgap the way some Congolese and Angolan cargoes were, so there’s more underlying demand holding their price up even once the emergency buying stops.

If the world did have too much oil, the size of the price fall in each country would be roughly in-sync, adjusting for things like oil quality and shipping cost, not on how much of that country’s recent demand was really just a temporary substitute for Gulf oil. Yet the latter is exactly what we saw: Congo and Angola, which were bought almost entirely as substitutes, have fallen the most. Nigeria, which has other buyers and uses beyond that emergency demand, has fallen by much less. That pattern only makes sense if this is one temporary cause unwinding at different speeds in each country, not evidence of a real global surplus.

The US SPR has fallen to 326 mb, the lowest since May 1983, and US commercial and strategic crude inventories combined dropped to 743 mb, the lowest since 1984. That is not what a market drowning in oil looks like. If the world were actually oversupplied, the US Government would be buying oil at these prices to rebuild its reserve, not still running it down.

Yet that’s exactly the contradiction in Washington’s behaviour. In 2025 the US had been refilling the SPR, buying at $79 a barrel, or below. That policy was paused on 11 March 2026, when the Energy Department redirected the reserve into releasing 172 mb as the US share of the IEA’s coordinated wartime response – a release scheduled to run roughly 120 days, putting it on track to finish right about now. Prices now are below the $73-79 range the government was previously happy to buy at. If officials believed this was a lasting surplus, the obvious move would be to finish the emergency release and go straight back to buying at an even better price than before. Instead, the reserve is still being drawn down, not refilled. That does not prove officials think the current price is wrong as the release was already scheduled to run its course, but it does sit uneasily alongside the claim that the physical market is already drowning in surplus crude.

Product markets are sending the same mismatch signal from another angle. The 3-2-1 crack spread – the standard measure of refining margin on gasoline and heating oil – has continued climbing through early July. The gasoline calendar spread has strengthened to levels last seen during the acute phase of the war, while the equivalent crude calendar spread has turned negative for the first time this year. Refiners don’t typically earn margins like that in a market drowning in crude, as an actual global surplus would be expected to show up as weakness in both crude and the fuel made from it, not a growing gap between the two.

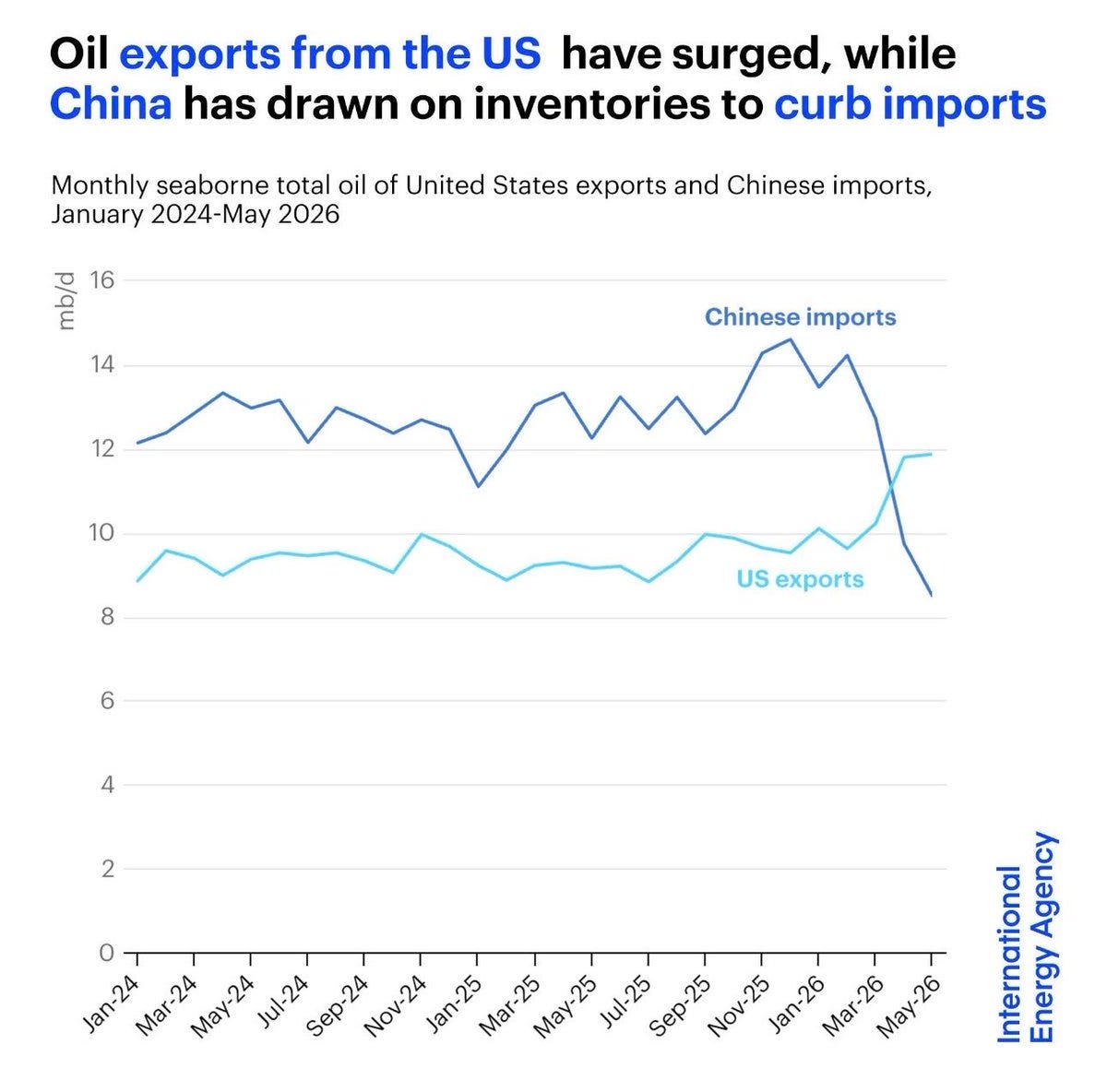

Morgan Stanley has argued the surplus is here to stay because of what they call two “solvers” – high US exports and low Chinese imports – that let the market absorb the Hormuz disruption without prices spiking as much as feared. The scale involved is substantial: IEA data shows Chinese seaborne imports falling from roughly 14.2 mb/d in March to about 8.6 mb/d by May, while total US oil and product exports rose over the same stretch by about 2 mb/d to nearly 12 mb/d. So it’s accurate in terms of total aggregate oil and product flows, but most of the extra US oil is light and sweet, while the disrupted Gulf oil is mostly medium and sour. These are different grades that most refineries can’t simply swap for each other. Counting US flows as a like-for-like replacement for Gulf crude overstates how interchangeable they actually are. Further, this relies on the bold assumption that lower Chinese imports are a permanent phenomenon, rather than temporary while drawing on reserves – there is no evidence to support this paradigm shift to lower imports.

Goldman Sachs and Citi both expect a surplus by 2027 – Goldman estimates roughly 3 mb/d before global reserves are rebuilt and 2 mb/d after, and Citi has flagged the possibility of Brent returning to $60 by year-end as Hormuz traffic normalises. Worth noting, though, that investment banks have a professional incentive to cluster around similar forecasts, since being wrong together costs a career far less than being wrong alone, so multiple banks agreeing isn’t as strong a signal as it looks. The evidence this piece actually relies on is the OPEC production numbers, global reserve and inventory levels, and the rates of loading, return and transit of tankers, all measured by tracking firms and government agencies, not forecast by banks with a reputation to protect.

What looks like a global glut is actually two finite mechanisms and one open question, not a sustainable surplus. The US strategic reserve releases and the Gulf’s wartime backlog are both one-off and both draining on a timeline that can be estimated, and both are close to their end dates now. China’s absence is doing the rest of the work in making this look like a glut, and its duration isn’t knowable the way the other two are.

Whether this stays a temporary distortion or becomes something the market has to take seriously depends on the race between two things: the disappearance of the drawdowns, the backlog and China’s absence, against the return of normal production, and loading and transit flows to fill the gap they leave behind.

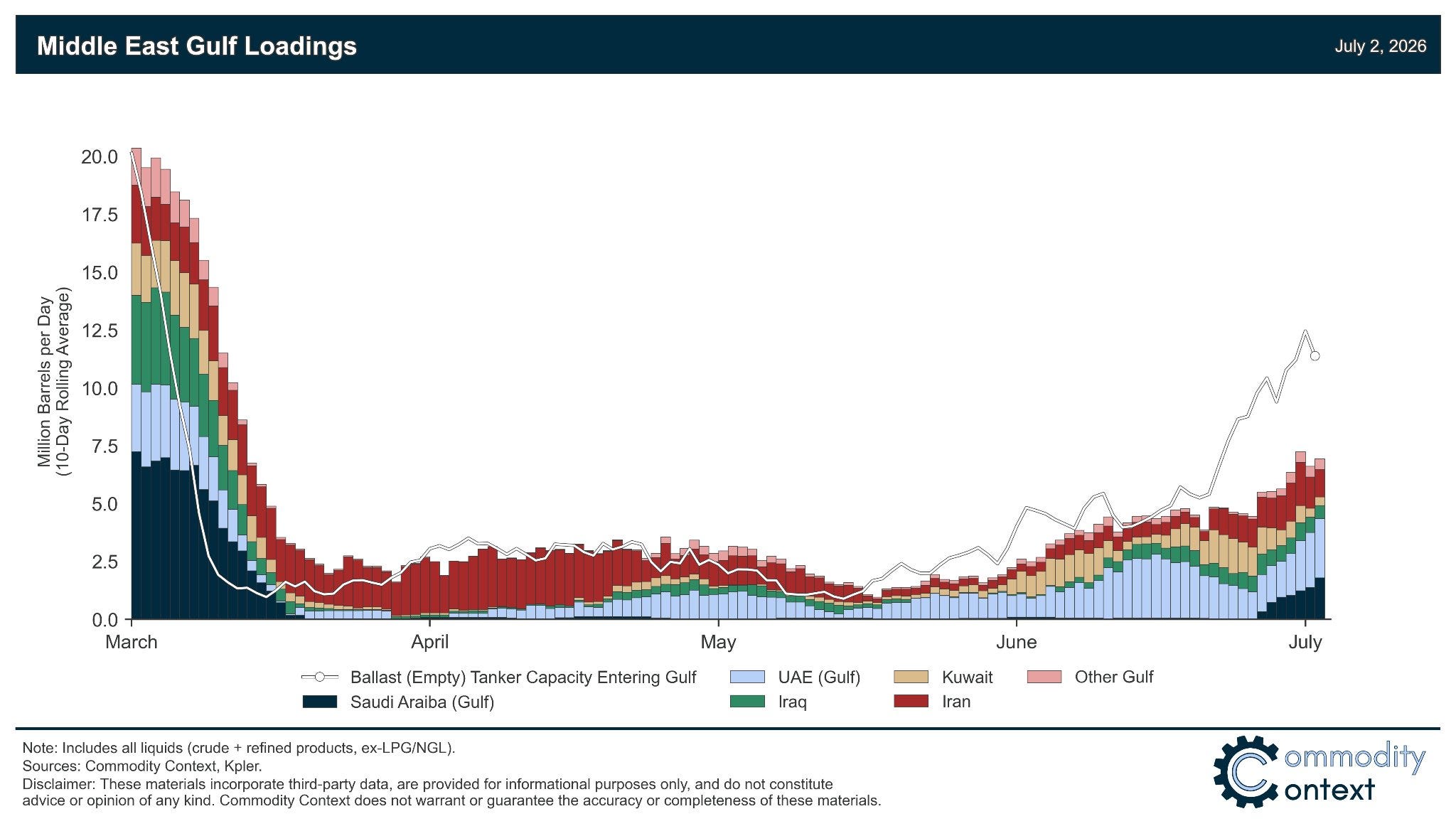

OPEC+ approved a further 188 kb/d target increase from August on 5 July – a figure small enough, against total OPEC+ output of around 40 mb/d, to be virtually a rounding adjustment. Yet feeling the need to increase production – even such a tiny one – is not a sign of confidence in a lasting surplus. Even the most recent supply-side headline doesn’t move the physical picture much. On the second part of the race Rystad Energy – an independent energy research and consulting firm – expects about 85% of the lost Gulf production volume back by early in the fourth quarter and all of it by January 2027. That is consistent with the trajectory discussed in Counting Barrels, but those timelines are not guaranteed because recovering production won’t count for much if the oil can’t regularly get out.

Transit through the strait continues to be a useful illustration of how unsettled this situation remains. Total traffic remains well below the pre-war norm of roughly 130-150 ships a day, while commodity-vessel crossings have recovered only unevenly and remain sensitive to which route is being used. That fragility was particularly apparent in the first days of July. Over 3-4 July, at least eight vessels attempting the Omani route reversed course, four of them then shifted toward the Iranian route and exited the strait, before Omani-route traffic partially recovered by the end of the weekend. Nothing about the underlying 60-day deal changed in that window – nobody renegotiated anything, no new agreement was struck, and no official explanation was given. Ships just stopped then started again; the disruption and recovery happened on their own, which is exactly the kind of unpredictable friction market is ignoring on the normalisation side of the race as current prices assume Gulf flows keep recovering smoothly before the backlog and reserves run out.

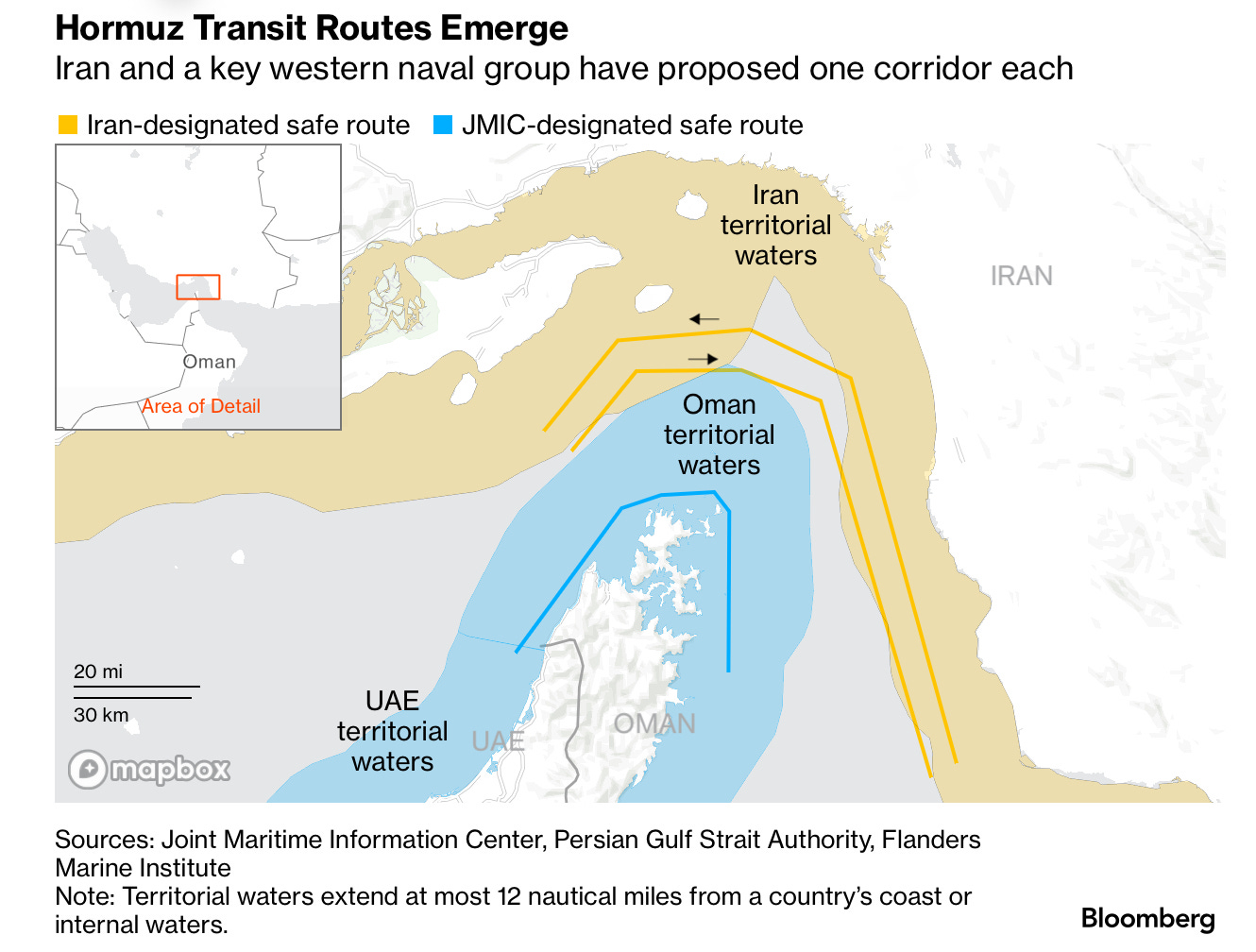

Iran continues to assert its control over the strait, forcing ships toward its own designated channel and leaving other routes subject to unresolved issues like mine-clearing and security assurances. The question of tolls once the current 60-day free-transit window ends likewise remains unresolved. There’s no agreement yet on what happens once the fee-free period expires, and Washington has previously indicated that paying tolls to Iran’s Government would itself be a sanctionable act, leaving shipowners exposed if Iran revives tolls after the window closes.

If Iran uses that leverage to slow or tax the return to normal flows, the production recovery Rystad projects doesn’t translate into the market normalisation the current price assumes. These uncertainties could result in the backlog and reserves disappearing before real flows are back, opening a gap the market currently has no reason to expect, because it isn’t pricing this as a race with an uncertain second leg at all.