Damage, Not Collapse

The blockade creates real pressure. The question is whether Washington can sustain it long enough for that pressure to matter.

The FT reported this week that Iran will have to start significantly reducing oil production within about a fortnight if the US naval blockade succeeds in choking off its exports. Storage tanks are just over 51% full, leaving a margin tight enough that the constraint becomes binding well before diplomacy resolves it. The logic is straightforward: blocked exports mean tanks fill, full tanks force production cuts, and production cuts carry a serious risk of permanent reservoir damage, unevenly distributed across fields, and operationally difficult to avoid under time pressure. That is real pressure on Tehran, and the timeline is short enough to force decisions in days rather than weeks.

There is a popular version of this story that goes further and gets it wrong. Iran’s oil exports are the key, the argument runs – shut them off and the economy collapses, the regime buckles, and a deal follows. It keeps circulating, and it consistently misreads how economic pressure actually works on a sanctions-hardened state. When people say Iran will “run out of money”, they are imagining something like a household that can no longer pay its bills, where income stops and obligations cannot be met. Sovereign governments with their own currency don’t work that way – the consequence of depleted foreign exchange is import compression: fewer goods, higher prices, more shortages. That is genuinely damaging, but it is a different thing from systemic collapse, and the distinction matters enormously for how the blockade’s leverage should be understood.

Iran has been living under varying degrees of oil export restriction for decades. The 2018–19 maximum pressure campaign cut exports sharply – from around 2.5 million barrels a day to well under a million – and the economy took a serious hit. Inflation spiked, the rial collapsed, living standards fell hard. Yet the regime adapted and survived, keeping the state functioning. The population absorbed the punishment and the government did not fall.

The reason Iran can absorb this punishment lies in how its import structure has been reshaped. Sanctions have compressed discretionary imports over a decade – consumer goods and luxuries were the first to vanish. What remains is mostly intermediate goods: industrial inputs, components, chemicals, and materials that keep domestic production running. These are hard to replace, which is why export pressure causes real damage through input-cost inflation and output contraction. But Iran has spent a decade building workarounds –grey-market channels, third-country intermediaries, rerouting trade, and domestic substitution where possible – precisely because it has operated under this pressure before. The coping infrastructure was built by the same sanctions that created the vulnerability. A less-adapted economy would face an acute crisis; Iran faces a worsening of a chronic condition it has already learned to manage.

The Offshore Buffer and the China Variable

Richard Bronze at Energy Aspects estimates that Iran has around 150 million barrels already loaded on tankers outside the Strait of Hormuz. Those barrels can still be sold, and they extend Iran’s revenue stream by weeks even after onshore production cuts begin. More importantly, they reveal what the blockade actually is: not a classical naval interdiction that physically stops oil moving, but a sanctions enforcement contest in which the US must deter and punish buyers rather than simply stop ships. Converting storage pressure into financial pressure requires Beijing’s cooperation – and beyond that, it requires the US to escalate horizontally through financial, legal, and interdiction channels, not just physically. That is a materially different and harder task than the blockade’s naval framing implies.

China purchases more than 80% of Iran’s oil exports, and Treasury Secretary Bessent confirmed on April 14 that the blockade is specifically designed to prevent Chinese vessels from accessing Iranian oil. One sanctioned Chinese tanker has tested the blockade perimeter already, but turned back. China’s incentives are mixed. Chinese refiners benefit directly from discounted Iranian crude, but state-linked financial institutions facilitating Iranian transactions face secondary sanctions exposure. Compliance with US enforcement would require Beijing to actively constrain its own firms – a political concession. Yet there is no public indication Beijing intends to wear that cost. The pressure mechanism only bites fully if Chinese buyers change behaviour, and that remains undemonstrated.

The 19 April expiry of the US sanctions waiver on Iranian oil is the immediate trigger. Two US officials confirmed to Reuters on 14 April that Treasury will enforce sanctions after that date, making the blockade and financial pressure simultaneously operational. That is the moment when the revenue squeeze becomes concrete rather than theoretical, and when the enforcement contest over Chinese compliance becomes the central variable.

The Islamabad Failure

The Islamabad talks confirmed what the structure of the problem already implied. Vance identified the single sticking point – Iran must commit to abandoning nuclear enrichment capability – and Araghchi said the two sides were inches from understanding before encountering “maximalism, shifting goalposts, and blockade”. Iran’s Parliament Speaker added that the US “ultimately failed to gain the trust of the Iranian delegation”, which points to the second structural barrier that most analysis underweights.

The US withdrawal from the JCPOA in 2018 destroyed whatever framework credibility existed, and that precedent alone gives Tehran reasonable grounds for scepticism about US commitment to any new agreement. The enrichment argument compounds this – as argued in The Prestige Bomb, Iran’s nuclear programme is not a weapons sprint but a sovereign insurance policy, and the Libya and Ukraine precedents taught any watching government that states which surrender latent nuclear capability lose their primary deterrent against regime change. Giving up enrichment means giving up the one capability that makes military action prohibitively costly, and no Iranian government can accept that domestically regardless of what economic pressure is applied.

Nuclear talks thus have two likely functions, neither of which is resolving the enrichment question. They give both sides a face-saving pause – Iran buys time on the storage clock, the US avoids the escalation decision while maintaining domestic political cover – and they allow both audiences to be told that diplomacy was tried. The Deal That Keeps Not Happening identified this dynamic before the war began; Islamabad confirmed it in real time.

The Strategy Washington Keeps Misreading

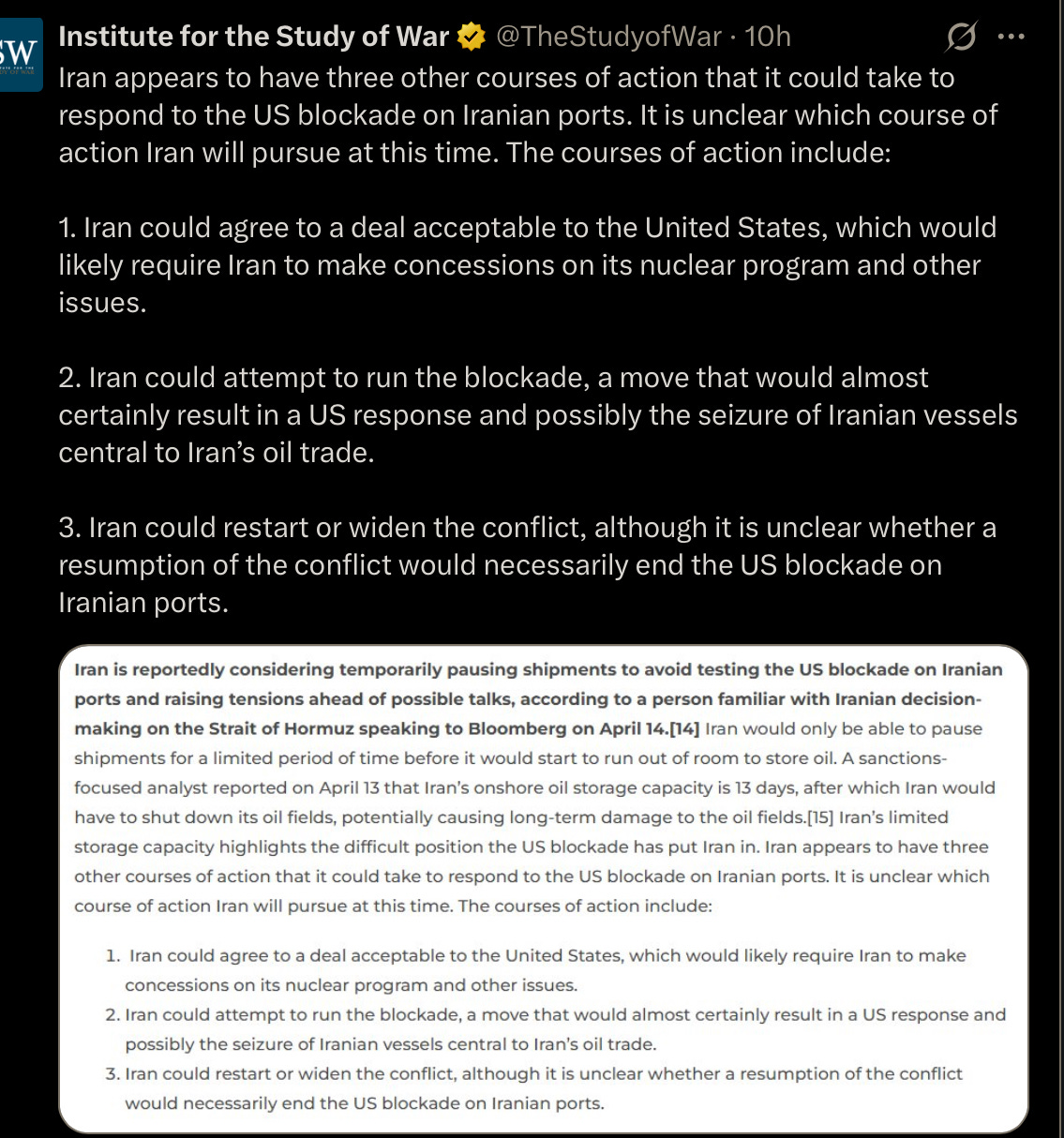

The Institute for the Study of War has framed Iran’s options as three discrete choices: agree to a deal, run the blockade, or widen the conflict. It is a reasonable taxonomy but a constraining one. It treats Iranian decision-making as a forced selection between alternatives rather than recognising that Tehran can pursue all three partially and simultaneously – appearing to negotiate, allowing some tankers to surreptitiously test the blockade perimeter, and activating Houthi pressure on the Bab al-Mandab without formally ordering it – while the clock runs on US political patience. A US strategy premised on forcing a discrete Iranian choice will consistently misread partial compliance as movement toward resolution.

This is ‘survive-and-exhaust’ applied to a blockade rather than a bombing campaign, and it is the doctrine Iran has been refining for decades, as argued in Who Is Actually Winning the Iran Campaign. According to ISW, citing Arab officials who told the Wall Street Journal on 14 April, Iran is already pressuring the Houthis to close the Bab al-Mandab, which would expand the economic cost of the standoff well beyond Iran’s own position and threaten Saudi oil exports redirected through the Red Sea.

The troop surge – 10,000 additional US service members arriving before the end of April, including a second carrier group and the 11th Marine Expeditionary Unit – is best understood as optionality rather than decision. Washington is maintaining capacity for additional strikes or ground operations while simultaneously pursuing further talks before the ceasefire expires on 22 April. That is the posture of an administration that does not yet know which way it is going, and it is consistent with the Goodfellas model identified earlier: the threat must remain credible without the act being taken, because the act forecloses options the threat keeps open.

The Cost Runs Both Ways

Bronze’s own conclusion in the FT is pointed: “the administration is unlikely to be able to afford to wait”. That is the asymmetry the damage-not-collapse framing makes legible. The blockade creates escalating pressure on Iran – real, measurable, accelerating after 19 April – but sustaining it long enough for that pressure to compound requires Trump to weather oil above $100 a barrel against a domestic backdrop already managing tariff-driven inflation, equity market volatility, and recession risk.

The macro context makes this harder still. As argued in Three Withdrawals Running Simultaneously, the Iran shock is landing in a global financial system under pressure from simultaneous liquidity withdrawals from Japan, the GCC, and China through independent channels that monetary policy cannot fully offset. The IIF has identified an inflection point at which the price response to supply shortfalls becomes convex – where thinning inventory buffers mean the same-sized disruption produces progressively larger price increases as the cushion disappears. A prolonged blockade doesn’t raise the oil price linearly; it risks a step-change in the price environment that makes Trump’s domestic position significantly harder to hold.

The blockade is a genuine escalation and a real source of pressure. The storage constraint is near-term and binding, the reservoir damage risk is a serious and escalating one, and the post-19 April sanctions enforcement makes the financial dimension operational. None of that should be confused with a mechanism that will break a sanctions-hardened state quickly enough to matter within Trump’s political window.

The enrichment gap is structurally unbridgeable under current conditions. The trust deficit means Iran cannot accept US commitments even if a formula were found. And survive-and-exhaust means Tehran’s optimal play is to absorb damage, manage the internal consequences onto the population, and wait for Washington’s patience to run out – which is exactly what Chatham House’s Sanam Vakil meant when she said this is a “test of wills”, and Iran has more practice at enduring them.

The blockade alone doesn’t resolve this. The US either escalates to a level that fundamentally changes Iran’s operational calculus, finds a diplomatic formula that papers over the enrichment impasse without resolving it, or runs out of political room and backs down. The troops are being positioned, the talks are continuing, and the ceasefire expires in six days. After 19 April, the sanctions enforcement contest and the storage clock run simultaneously – and at that point, the ambiguity Washington has been managing becomes a decision it can no longer defer.